Article | Apr 2019

Ten Years of Say-on-Pay Data Show Your “Against” Vote is Coming

Data highlights the potential exposure companies have to negative votes from proxy advisors. Strategic shareholder outreach can be the antidote.

We researched 10 years of say-on-pay proxy advisory recommendations and results to understand how common it has been for a company to receive an “Against” vote recommendation or low say-on-pay support in a given year. The results are illuminating; more than 40% of Russell 3000 companies have received an “Against” vote recommendation from ISS, and almost half have received low say-on-pay support. The trend also suggests that these percentages will continue to increase each year. Therefore, we believe companies would be well served to conduct regular, proactive stockholder outreach and engagement to mitigate the impact of a future negative vote recommendation.

The end of 2018 marked the 10-year anniversary of mandatory say-on-pay (SOP). Admittedly, the first two years were limited to financial institutions that received capital under the Troubled Asset Relief Program (TARP), but nonetheless this is an opportune time to evaluate how things have transpired over the past decade.

Say-on-pay first entered corporate America when, in early 2009, Treasury Secretary Timothy Geithner stated that recipient banks of TARP relief must hold SOP votes. By 2011, a vast majority of public companies across all industries became subject to these votes, triggered by President Obama’s signing of The Dodd–Frank Wall Street Reform and Consumer Protection Act on July 21, 2010. Today, SOP votes are as routine as the annual meetings in which they take place.

There have been many studies covering the frequency of negative say-on-pay votes, and the impact of negative shareholder advisory voting recommendations on actual vote outcomes, but we have yet to see a study on how common it has become for:

- Companies to have received an “Against” vote recommendation from a proxy advisor in their history; and

- Companies to have received suboptimal shareholder support (defined as less than 85%) in their history.

This is a potentially important frame of reference to evaluate your own company’s results. Management teams and compensation committees are loath to receive an “Against” vote recommendation from a proxy advisory firm. However, due to the structure of the models and evaluation approaches used to determine support of the say-on-pay proposal, it very well may be the case that the vast majority of public companies will eventually receive an “Against” vote recommendation. To research this, we collected Institutional Shareholder Services’ (ISS) SOP vote recommendations and SOP voting results for Russell 3000 members from 2009 to 2018.

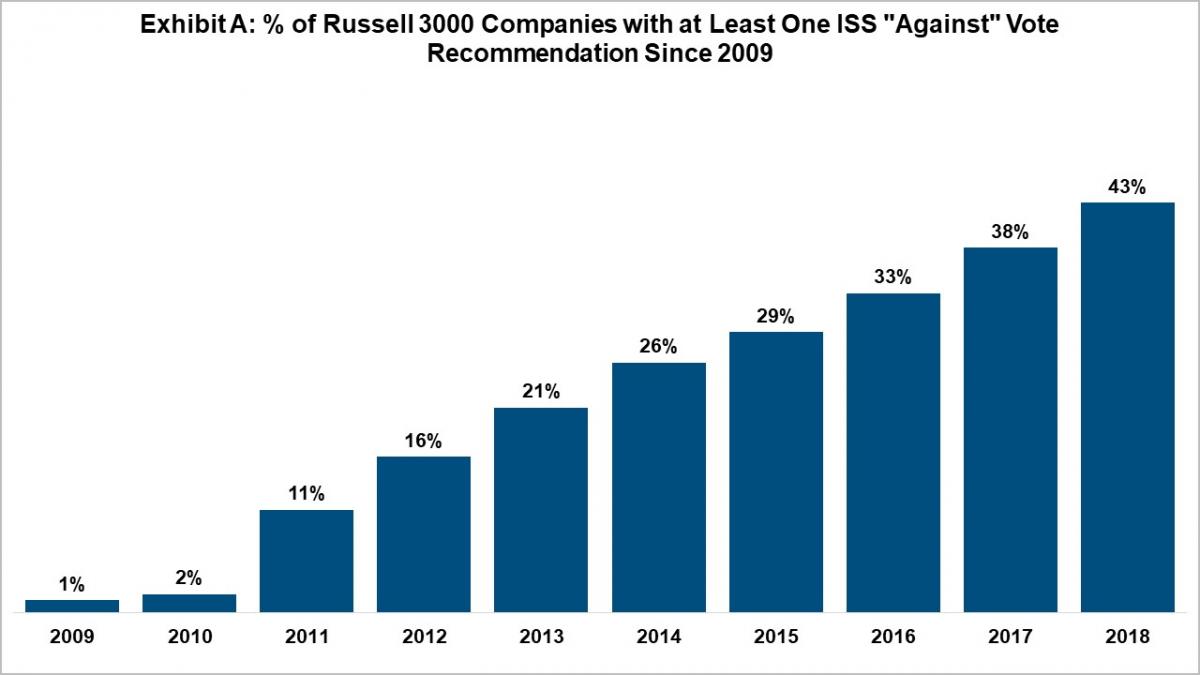

Exhibit A below shows this “build” where each year the number of companies that have received an “Against” vote recommendation from ISS in their history grows. We expect this growth to eventually level off as some companies have dynamics that will always fare well against the proxy advisory models (think of the founder-CEO who does not receive any long-term incentives). However, this levelling-off point is not anticipated in the near-term, and this number will certainly continue to trend upward for a while longer. It is reasonable to expect that at some point in the future, more than 80% of companies will have fallen victim to a negative vote recommendation at least once.

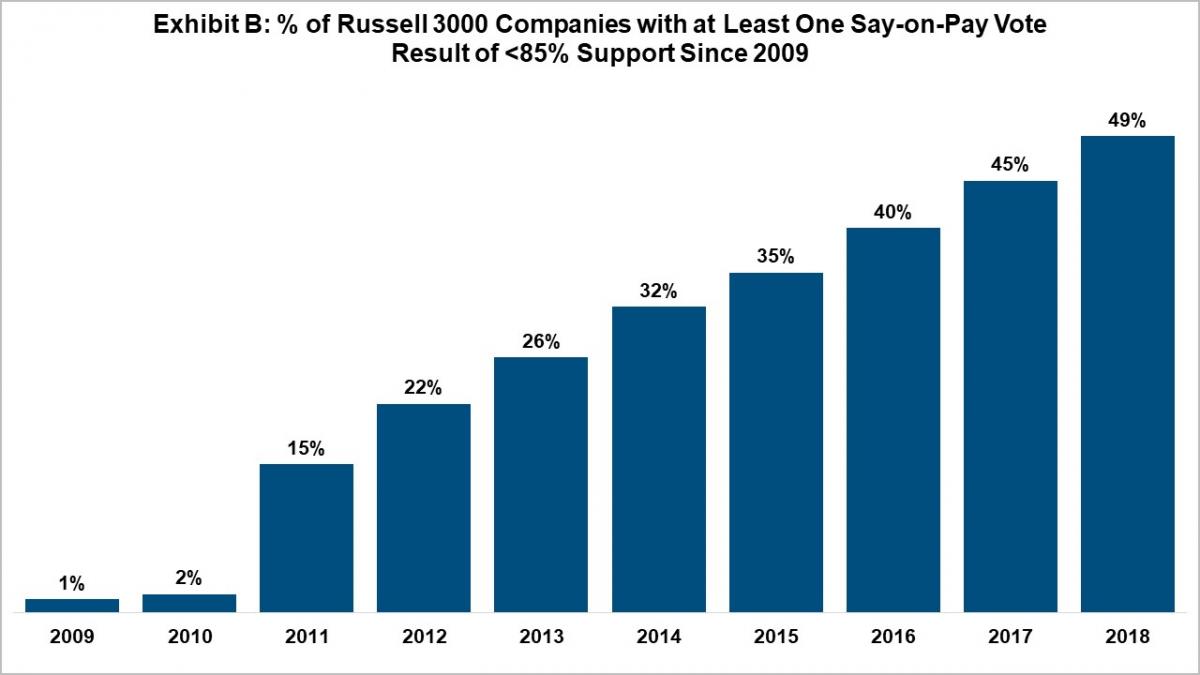

While Exhibit A is limited to data for the past 10 years on ISS say-on-pay vote recommendations, ISS is not the only influential proxy advisory firm. Unfortunately, we do not have 10 years of results from firms like Glass Lewis & Company, so we have used suboptimal shareholder support on say-on-pay (<85%) as a barometer for companies that have received an “Against” vote recommendation from any one of the major proxy advisory firms. Similar to Exhibit A, Exhibit B shows the buildup of companies that have received suboptimal support at least once over the past 10 years. As you can see, when making evaluations through this lens, we see that about half of all Russell 3000 companies have experienced a negative vote recommendation.

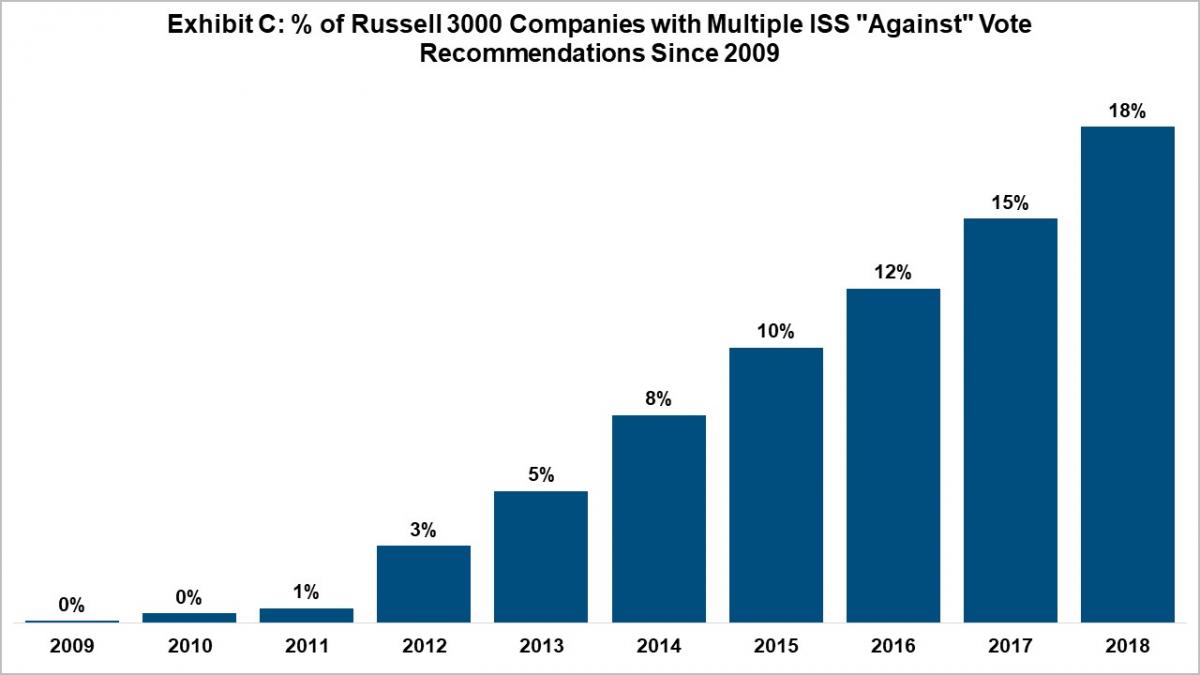

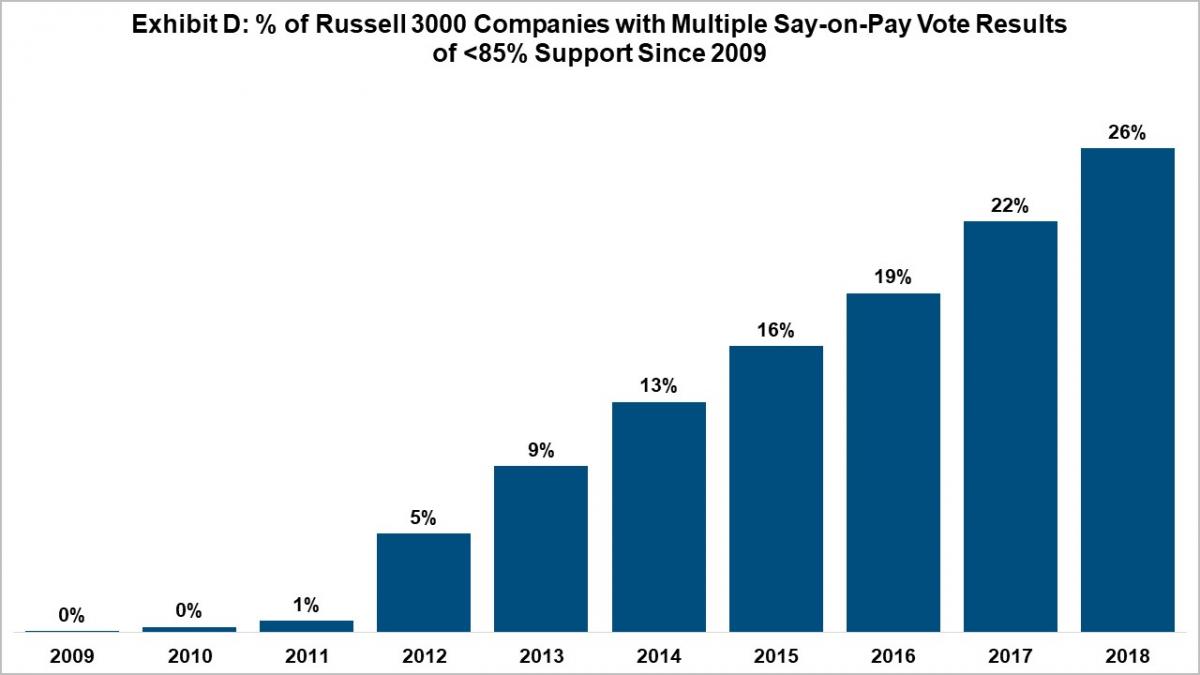

Another interesting area to explore is the likelihood of multiple negative vote recommendations or multiple years of suboptimal support. Cases of “multiple failures” with respect to both recommendations and vote outcomes are not uncommon. By 2018, about one in five (18.4%) Russell 3000 companies had experienced more than one ISS “Against” recommendation, and more than one in four (26.4%) had received lower than 85% say-on-pay support multiple times. Exhibits C and D below illustrate trends with respect to multiple negative outcomes; the increase has been substantial since say-on-pay votes began, and no pattern of leveling off or decreasing is evident.

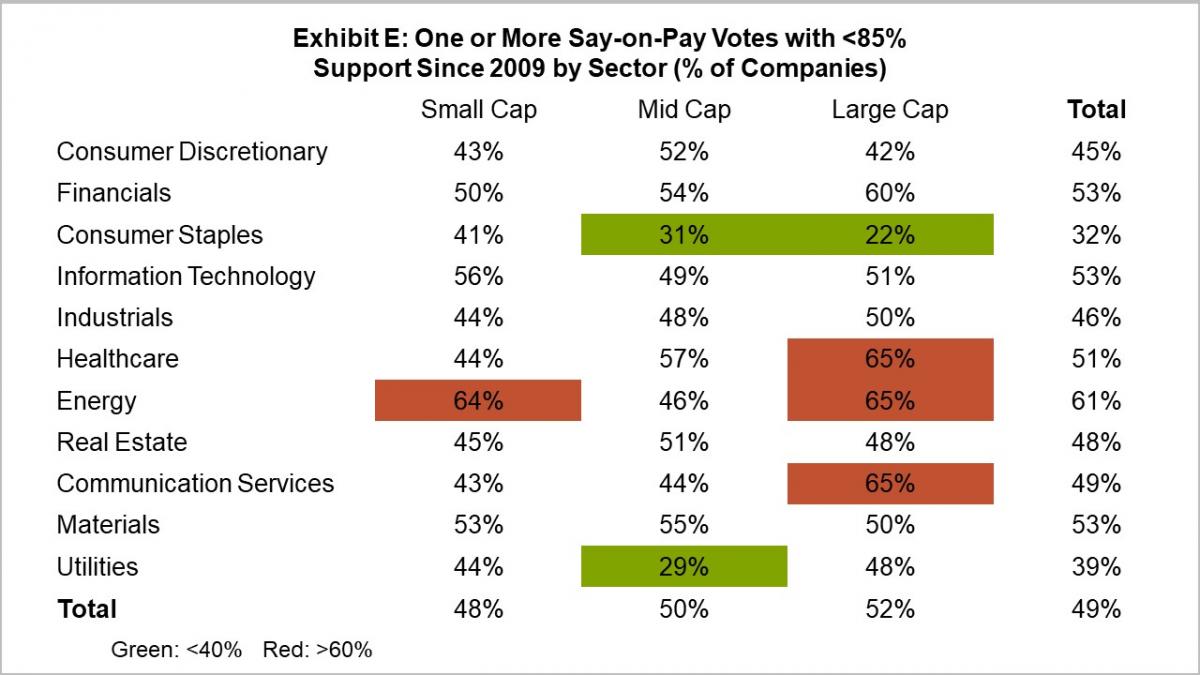

We also researched variations and patterns in the results by industry sector and company size. More instances of less than 85% say-on-pay support occur as company sizes increase: 48%, 50%, and 52% of Small, Mid, and Large Cap companies, respectively, have had at least one occurrence of less than 85% SOP support since 2009. Additionally, the three size/sector segments with the highest occurrence of <85% support are all of the Large Cap group: Large Cap Health Care, Energy, and Communication Services.

Some sectors have it easier than others. Consumer Discretionary, Consumer Staples, and Utilities have relatively low prevalence of under 85% SOP support, across all size groups. Typically, however, rates fall between 40 and 60% for each size/sector segment. Please refer to Exhibit E, below, for more detail.

Implications and Recommendations

These findings highlight the potential exposure that companies have to negative vote recommendations from proxy advisors. To counterbalance this risk, companies should escalate the importance of shareholder outreach and engagement. Many companies currently perform annual governance- and compensation-related outreach and engagement, but for those who have not yet undertaken this exercise, consider the following key steps as a baseline:

- Define the scope of the outreach. This covers (i) who the company would like to reach out to, and (ii) what the purpose of the outreach should be (i.e., just compensation, compensation and governance, etc.).

- Define the outreach team and their associated roles. In our experience, outreach efforts are typically led internally by the Head of HR, General Counsel, and potentially the CFO. With certain significant stockholders, a member of the board—often the lead director or compensation committee chair—may participate. In many cases the company’s proxy solicitor and outside compensation advisors are also involved in the strategy and execution of the process. There is also a team of people that supports this group from an operational perspective.

- Understand your stockholder voting guidelines before engaging with them. Most of your large, significant stockholders will have their own internal policies on how they evaluate compensation and governance. In addition, tools are available that can provide insight into how closely these stockholders follow the main proxy advisors.

- Develop materials to serve as a conversation starter. Before the company engages in discussions with stockholders, develop a set of slides that cover the key points of the topics to be discussed. Typically, these materials represent a summary of what is already available to the public (generally through the proxy statement, 10-K, or 8-Ks). Keeping to publicly-available information avoids inadvertent disclosure of material non-public information. The goal of these slides is to provide some background on the company, key highlights of the program, policies, decisions, etc. so that stockholders can have an informed opinion going into the discussions and can provide constructive feedback.

- Disclose your outreach and engagement efforts. In each proxy statement, disclose the summary points of your outreach efforts. For example:

- How many stockholders did you reach out to?

- How many agreed to talk with you?

- Who from the company participated in the discussions?

- What were the key findings and themes?

- What, if anything, did the company do to address those key findings or themes?

Going through the outreach and engagement efforts proactively, even if the proxy advisors have been supportive and the company’s vote results have been good, can significantly benefit a company if or when a negative vote recommendation comes around.