Article | Apr 2018

Compensation Committee Outlook: Staying Nimble in 2018

Compensation committees must be alert to change and its potential risks. See our annual list of top five issues to address and recommendations to consider.

Pearl Meyer offers its annual Top Five issues for compensation committees. Boards are considering the impact and reacting to the changes brought about by tax reform, diminishing regulation, shifts in political and cultural norms, and an ongoing acceleration of change in business environments. Individually and collectively these factors are demanding that boards be alert and nimble.

We have identified five topics—a mix of practical and forward-thinking—that can help compensation committees address near-term concerns, get ahead of the issues that are gathering steam, and think about what might emerge in the future.

- The Silver Lining in Tax Reform for Executive Compensation

Compensation committees are considering what the repeal of 162(m) means in both the short and long-term. We encourage exploring the opportunity it provides to re-think and possibly re-design pay programs. - Three-Dimensional Pay Analysis: the Whole is Greater than the Sum of its Parts

There are three primary pieces of executive compensation plan analysis that when combined, can give committees a comprehensive picture of the value and long-term potential of their pay programs. - The Next Corporate Scandal Could be Yours: How to be Prepared

There are multiple near-term applications of the lessons learned from recent cultural debacles. Part of being prepared is ensuring that your executive employment contract terms and conditions support quick, decisive action and limit your risk. - Tech Talent is Everybody’s Business

Whether it’s related to operations or innovation and growth, it’s the rare organization that doesn’t need more tech talent. How can comp programs attract, retain, and grow the tech talent you need—at all levels of the organization, including the board—now and in the future? - Gender Pay Equality: Where ESG Meets HR

Environmental, social, and governance issues are gaining traction and investors are more and more interested. Gender pay equality, along with diversity of leadership, is getting top billing and companies face reputational, performance, and engagement risk by not examining how they can improve compensation parity.

The Silver Lining in Tax Reform for Executive Compensation

Executive compensation just became more expensive for public companies. The tax reform bill enacted in late 2017 included a meaningful change to section 162(m), a.k.a. the “million dollar cap” rule. Under the revised rule, compensation to Named Executive Officers (NEOs) in excess of $1 million is no longer a deductible expense for companies—even if that pay is “performance-based.” Furthermore, going forward this $1 million cap will cover more executives; it now applies to anyone who is or has ever been an NEO of the company.

Popular wisdom suggests that the original Section 162(m), enacted in 1986, was a largely ineffective attempt by Congress to put the brakes on what many believed was runaway executive pay. This time around, everyone seems to acknowledge that the changes are more about increasing government revenues than a new attempt to influence corporate governance.

That said, while the change in 162(m) will make senior executive compensation more expensive, over time we believe there may be positive implications for executive pay.

Enhanced Committee Discretion

Under the old rule, companies could only avail themselves of the “performance-based” exemption if (a) incentive payments were based on finite goals set by the compensation committee within the first 90 days of the performance period and (b) subsequent payouts could not be adjusted upward (i.e., no positive discretion). While committees have always had the ability to provide additional compensation outside of the 162(m) compliant plan, in reality few companies used this alternative, preferring to avoid unfavorable disclosure and tax consequences and potential negative shareholder response. As a result, we saw many committees spend inordinate amounts of time at the beginning of each year trying to anticipate all the potential adjustment factors that they might want to take into account in the bonus calculation. Then, at year-end, when the inevitable unanticipated event occurred, committees were left in the unenviable position of treating NEOs differently than other bonus-eligible employees in order to remain compliant.

We don’t expect, nor do we recommend, that companies eschew their current performance-based approach to incentive design. Even without 162(m), shareholders will continue to expect executive pay to be aligned with performance. But we believe the change in 162(m) treatment frees the committee to better exercise its business judgment—both positive and negative—without tax repercussions.

Better Pay Mix

While a number of large public companies long ago broke through the $1 million “cap” on salaries, we certainly saw the cap impact salary decisions for many smaller public companies. And, it is probably fair to say that the perceived limit on the more fixed, guaranteed elements of pay (salary and time-vesting restricted stock) resulted in higher, rather than lower, overall levels of executive compensation.

Over the next several years, we would expect to see companies re-thinking their pay mix based on business and talent strategies, rather than tax treatment. For example, the average CEO Target Total Direct Compensation package among Top 200 companies last year was roughly $15 million. Of that, only 9% was base salary. Does it really make sense for anyone’s target pay package to be 91% variable? Of course, 162(m) is only one of many factors that have contributed to the current trends in both the size and mix of executive pay packages, and the new rule won’t result in changes overnight. But treating all forms of compensation the same opens the door for new discussions about what the “right” pay mix should be.

Stronger Incentive Leverage and Performance Goal-Setting

Recalibrating the fixed-variable pay mix could also have interesting implications for incentive plan goal-setting. Although such changes would also require a fairly big shift in the way most American executives think about incentives.

In current US corporate culture, payout of some annual bonus amount has become an expectation. Zero bonuses are a rare occurrence, and zero bonuses for two consecutive years almost guarantees a change to the bonus plan, the management team, or both. As a result, in many companies the threshold bonus level has become almost a deferred salary payment (i.e., all but guaranteed). If companies were to re-think their salary levels (as noted above), then they could also re-think the role of incentives—especially annual incentives. If executives no longer expected a pseudo-guaranteed minimum bonus every year to supplement salary, companies could actually set more aggressive performance thresholds for their incentive programs.

For long-term programs the change in 162(m) also frees up companies to be more transparent. Currently, many companies set token performance targets on restricted share programs in order to qualify them as “performance-based” pay under 162(m). Going forward, companies will have more flexibility to include an appropriate level of time-vested restricted stock as an important retention component of their executive pay program, and then set meaningful performance goals for their performance share plans.

Three-Dimensional Analysis: The Whole is Greater Than the Sum of its Parts

The objective of any executive compensation program is to pay competitively, fairly, and consistent with performance. Yet many compensation committees place inordinate—even exclusive—reliance on traditional compensation benchmarking to assess their programs. While such benchmarking is important, alone it is inadequate. We believe a three-dimensional approach to executive compensation analysis can give committees much better insight for managing their executive compensation program.

Target Pay Analysis is traditional compensation benchmarking where we review salaries, target incentives, the grant value of long-term/equity awards, and the sum of these components (total direct compensation or “TDC”) against the market. Such benchmarking is useful to calibrate executive pay to a desired pay positioning goal (e.g., pay levels and pay mix are targeted to the market median). The analysis is widely understood and the basis upon which pay increases are determined each year.

But do market median pay levels and pay mix inevitably lead to fair pay outcomes and pay-for-performance? As most compensation committee members certainly know, they do not. When was the last time your company produced exactly on target financial results and the realized value of equity awards equaled the grant value? Variable pay exists because we know performance will vary—from total failure to spectacular success and all points in between. So, how can we know if the pay program will lead to the desired outcomes?

Pay Opportunity Analysis takes into account the range of potential outcomes above and below target financial performance, as well as stock price performance. The analysis takes into account pay mix and plan design features, such as different incentive plan threshold and maximum award levels. Two executives at different companies with exactly the same target pay can have very different pay opportunities for non-target performance results. The analysis may show that your company has a “flat” pay-to-performance opportunity profile relative to your peers—that is, threshold level performance delivers higher pay than the same assessed performance among peers, and superior level performance delivers lower pay than peers.

Conversely, the analysis may show that your company has a “steep” pay-to-performance opportunity profile, and greater downside risk and upside opportunity. Or it may show a mix of flatness and steepness above and below target. The analysis can also determine the relative sensitivity of your program to financial versus stock price performance variations and is valuable for incentive plan design and pay mix decisions.

Together, target pay analysis and pay opportunity analysis give a more fulsome picture of your pay program. But the range of pay opportunity says little about the difficulty of achieving any specific level of performance.

Pay-for-Performance Analysis examines actual pay and performance outcomes, typically over a three-year period. Ultimately, the results of such analyses will give the most definitive picture of the effectiveness of your executive compensation program. This view is not concerned with target pay levels, pay mix, plan design, or goal-setting philosophy, but measures ex-post pay actually earned and performance delivered, relative to peers. If your pay program is aligned and balanced vis-à-vis the first two analyses, but your pay-for-performance is misaligned, it is likely due to goal-setting issues. Tougher (easier) goals lead to more conservative (aggressive) pay-for-performance outcomes.

The shortcoming of this analysis is that it is a snapshot, capturing a single three-year view of your program. A subsequent three-year period may show a very different outcome relative to peers. Fortunately, the first two analyses can help committees understand how future outcomes are likely to appear.

Separately, each of these analyses provide useful, but incomplete information for executive compensation program management. Together, they provide a more complete set of insights to aid decision-making related to pay levels, pay mix, plan design, performance focus, and goal-setting. Three-dimensional analysis forms a solid foundation for a committee to ensure an effective program more likely to produce results that are competitive, fair, and consistent with performance.

The Next Corporate Scandal Could be Yours: How to be Prepared

There have been several recent high-profile corporate scandals resulting in significant declines in shareholder value and the departure of high-level executives. In these situations, boards are routinely criticized for insufficient response and ineffective compensation policies or practices. However, we believe these criticisms can be mitigated by proactive consideration of desired outcomes and the corresponding adjustments, if any, to certain compensation policies or practices. Even if no specific changes are made, completing this type of thoughtful, up-front review will enable faster and higher quality responses.

What should constitute a termination “for cause?”

Compensation committees should review and discuss the definition of a “for cause” termination. Whereas the ability to terminate “for cause” is conventionally limited to purely legal matters (e.g., conviction of a felony, fraud, embezzlement, etc.), many current definitions include provisions such as failure to fulfill assigned duties to the satisfaction of the board, Code of Conduct violations, and moral turpitude. Although many of these require judgment, the proper definition will allow boards to terminate executives involved in a scandal without paying severance or other benefits (e.g., accelerated vesting of equity awards) that are often provided upon a termination without cause. Furthermore, boards should discuss whether such events should impact existing retirement provisions, which could result in the responsible individual leaving the organization with enhanced equity benefits prior to the board having full knowledge of the situation and knowing the impact on shareholder value.

Should the clawback policy be triggered?

Most companies have adopted clawback policies. However, many policies are triggered exclusively by a financial restatement. Accordingly, an event that does material harm to the company and/or shareholder value, but does not require a financial restatement, would not allow for recoupment of incentive compensation under the clawback policy. Compensation committees should review their clawback polices and determine whether the triggers should be expanded to allow for recoupment under a broader set of circumstances that have resulted in a material decline in shareholder value. Even if such occurrences would allow for recoupment, the facts and circumstances of the event may not result in the board pursuing recoupment.

Are there appropriate stock trading restrictions in place?

As these situations unfold, executives are often in possession of material, non-public information. Accordingly, their ability to trade in the company’s stock should be restricted. However, even in cases where such policies were in place (such as pre-approval of all stock trades), the implementation of these polices had become routine or had been delegated to a level within the organization that was not aware of the concerns at the time approval was granted. Compensation committees should review their insider trading policies and the implementation of these policies (including approval, notification, and communication), to ensure that appropriate processes and restrictions are in place.

Compensation committees should also discuss whether these situations should trigger extended stock ownership and holding requirements post termination, otherwise, the terminated or retired executives may be the only executives that can minimize their loss by immediately selling their shares upon termination.

We acknowledge that you cannot plan for every circumstance, but we believe that having these conversations before an event occurs is the key to improving the speed, quality, and perceived “appropriateness” of board responses.

Tech Talent is Everybody’s Business

Is your company ready for the next wave of technological innovations and threats? Technology’s impact on business is exploding, which has intensified competition for tech talent and the need for creative compensation solutions, even outside the pure tech industry.

Market factors driving changes in business strategy include:

- Accelerated growth and innovation as companies prepare for the Internet of Things;

- Customer reliance on technology to acquire/consume goods and services;

- Opportunities to lead the market by using Big Data to predict business trends; and

- Greater severity and scope of cybersecurity risks to operations.

The concentration of tech companies in Silicon Valley has resulted in fiercely competitive compensation and benefits offerings, including higher cash, sign-on stock awards, 100%-company-paid healthcare, concierge services, commuting assistance, etc. As more traditional and tech-related companies also seek to hire tech professionals, all companies are facing challenges in attracting and retaining key tech talent.

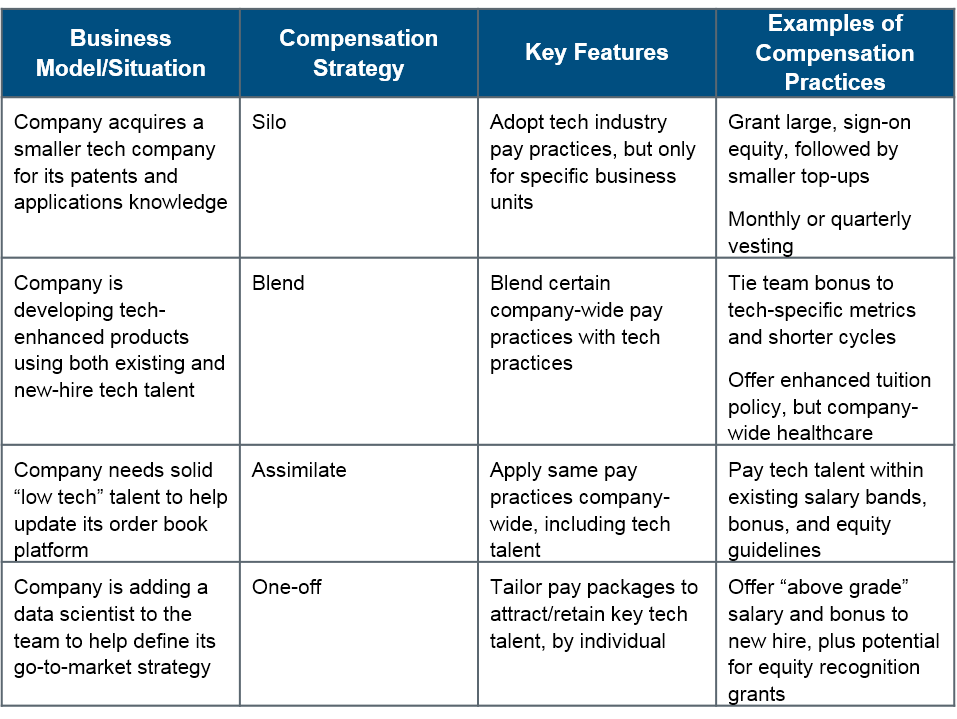

What is the best way to address disparities in pay practices for tech vs. non-tech talent? Compensation committees and human resources leaders should start by aligning their compensation and leadership strategies with their business model. Through our client experiences, Pearl Meyer has identified four main approaches:

These examples recognize that tech talent is not a homogeneous pool. Some skills and experience sets are in much greater demand, such as data science, cybersecurity, and digital transformation. Further, the ability to communicate well and manage across tech and non-tech business teams is a critical skill for senior tech leaders.

How tech talent is sourced also impacts the compensation offered. Consider the “GPA” of talent strategies: Grow, Poach, or Acquire (an entire business). A strategy of poaching candidates from Apple or Google may drive “one-off” packages. But turnover is high, so companies may need more generous education and development programs to grow their own and retain external hires. The “silo” approach may be best when acquiring businesses/talent. To quote a client’s CEO, “We don’t want the host antibodies to kill off the new venture.”

At the board level, many companies want to add a director with tech and cybersecurity experience. Since companies almost always offer the same compensation program to all directors, attracting a tech leader to join your board is about the opportunity to make a difference, their personal interest in the business issues, and networking. For example, the chairman role of an innovation and technology committee could be attractive to candidates.

Ultimately, tech professionals value work culture, job content, and career prospects. If compensation is the only attraction, it will usually take an excessive amount to attract and retain the best tech talent, either as an employee or a board member.

Gender Pay Equality: Where ESG Meets HR

Environmental, social, and governance issues are gaining traction as both a general concept and as documented key performance metrics. Investors are more interested in how companies fare in these areas and some, such as Blackrock, are increasingly vocal about their concerns.

Gender pay equality, along with diversity of leadership, falls into this broad category of newer measurements and it is certainly getting top billing in our cultural dialog. We are also hearing the topic discussed more frequently in the boardroom, spurred not only by current events, but also by new global regulations and emerging positions among proxy advisory firms.

- Numerous states, including California, Delaware, Maryland, Massachusetts, New York, Oregon, and the territory of Puerto Rico, have recently increased the robustness of their individual pay equality laws.

- The UK has adopted regulation requiring any company with more than 250 employees based in the UK to disclose their gender pay gap by April 2018.

- ISS will now evaluate requests for reports on a company’s pay data by gender or reports on a company’s policies and goals relative to gender pay disparity on a case-by-case basis. They will factor in a number of issues including whether or not a company has had recent controversy, litigation, or regulatory action related to gender pay.

- While it will not currently impact voting recommendations, ISS has also indicated they will highlight boards with no gender diversity.

What is less often discussed is the fact that this is not just a best-practices governance issue or a moral dilemma, it’s also a long-standing legal issue. Companies face real litigation risk along with reputational, performance, and engagement risk by not examining how they can improve compensation parity.

While there are a fairly large number of tactical avenues that human resources teams should be exploring now, boards cannot afford to be passive in this area. If one does not exist already, we suggest adopting a policy on gender pay equality that sets a clear expectation for company action. Explicitly state the company recognizes the issue as critically important and that the organization is committed to open dialog and improvements where and as needed. Boards can also outline their near-term milestones for management, which may simply be necessary data collection and an assessment of the company’s current position, before outlining steps for progress. Finally, recognize that the focus on gender pay equality is about more than just equal pay for equal work. It’s also equal opportunity. Any comprehensive review of pay equity should also include an analysis of workforce demographics by organizational level, as well as an overview of succession planning strategies and diversity.

Conclusion

While we believe these five points to be timely considerations for compensation committees, we note that the importance of “business as usual” items such as aligning pay to strategy, managing compliance and regulation, and developing effective leadership teams for the long-term has not waned but has in fact, become more complex.

Today’s board is critical to the success of a public company and offers directors an opportunity to affect considerable change. Just as we suggest compensation plan design can be a differentiator in the attraction, retention, and motivation of executives, a vigilant and flexible compensation committee can likewise make a significant positive impact on the board at large and its guidance of an organization.