Advisor Blog | Oct 2023

Setting Annual Incentive Compensation Goals in Biotech

It’s a fundamental question: Should the annual bonus structure rely on execution-based or results-based goals?

One of the most challenging compensation-related items that boards and management teams work through is the goal-setting process for the annual cash incentive plan. In most industries, companies have commercial products or services that generate financial results which can be measured and used as the basis for incentive funding purposes, are the primary value drivers for the company, and are the way its performance is gauged externally. It is quite different in the biotechnology sector where the key value drivers are often non-financial and geared toward making scientific or technical progress toward commercial products at some point in the future. This is entirely the case for precommercial companies, but holds true for larger commercial organizations as well.

Whether a therapy is viable depends on high standards around safety and efficacy, which are arguably outside of management’s control. These factors suggest that management execution plays an important role in driving toward success in biotech, but ultimately the scientific results will determine whether a company is successful and able to achieve its mission.

Therein lies one of the fundamental questions in developing incentive goals in biotech: Should they be based on management execution (i.e., inputs) or the actual scientific results (i.e., outputs)?

The Basics in Biotech Incentive Design

Short-term cash incentive programs in precommercial biotechnology or life science companies tend to follow a similar structure. There are a number of key scientific, operational, financial, and organizational goals that are weighted according to their relative importance to the company in a given year. Typically, scientific goals represent a large majority of the overall weighting, followed by financial (e.g., raising funds on favorable terms) or operational depending on the company’s needs, and then organizational. The methods to evaluate whether a company partially achieved, achieved, or overachieved relative to those metrics can differ by company, ranging from pure discretion to actual definitions of what constitutes achievement along the spectrum. The compensation committee and management team evaluate the results at the end of the year based on scoring each metric and applying the attributed weighting. Those individual scores are then added up to arrive at an overall corporate score.

The Challenge with Setting Goals

One of the key philosophical decisions that underlies the goal-setting process is whether the goals will be set up to be based on execution of a particular set of tasks, or the results of the topic at hand. Below is an example that illustrates the point:

| Goal Theme | Execution-Based | Results-Based |

|---|---|---|

| Progress Asset ABC | Fully enroll ABC study by June 30 | Positive data read-out from ABC study |

You could envision that the incentive funding results could be quite different based on an execution-based goal versus a results-based goal.

The Case for Execution-Based Goals

Management teams will typically prefer to have execution-based goals because they have greater influence and control over meeting the objectives and earning the associated bonus dollars. From an incentive theory perspective this is the preferred design method because the goals will drive behaviors and provide motivation. Results-based goals cannot do so to the same extent since the individual or team ultimately does not have complete control over the outcomes. The execution-based method is also beneficial from an employee retention standpoint because even if a drug or technology were to fail in achieving the desired safety, efficacy, or technological result, if the execution of that testing or process was done well then incentives could still be earned.

The Case for Results-Based Goals

Results-based goals may not have the same line of sight as execution-based goals, but they are generally more tightly linked to stakeholder goals. In this instance it would be stockholders, in the form of increased stock prices should the results of a study be positive, or patients, where positive results bring patients closer to having a therapy or medicine for their disease.

A Hybrid Model for Consideration

One possible conclusion is that there should be some hybrid design that effectively drives execution on the goals, and also rewards individuals and teams for positive clinical and technological outcomes. An approach that we believe achieves this is to create goals that provide the participants the ability to earn up to 100% of their bonus based on the execution-based outcomes of the respective goals, and only in the event that the outcomes are also positive would the participant be able to earn an above-target bonus. This balances the needs of the organization (motivation and retention), with the needs of stakeholders (incentivizing results).

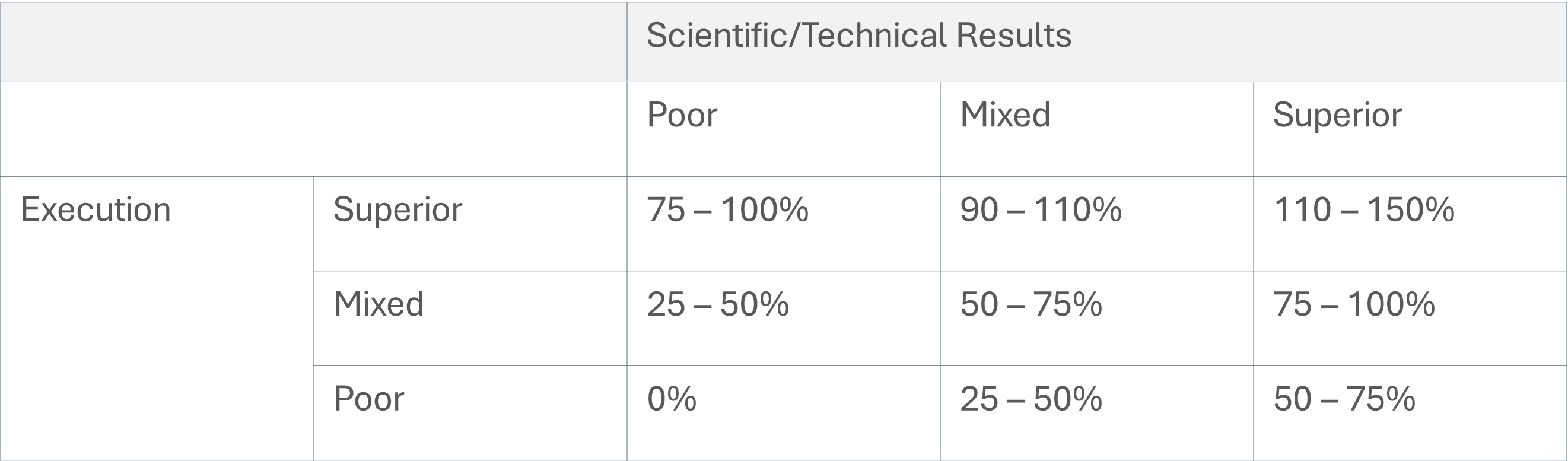

Testing the Overall Rigor of the Plan

Below is an illustration of incentive funding ranges under different execution- and results-based outcomes. It could be used as a guide to back-test the draft incentive plan goals to understand if the funding outcomes are roughly in line with these rules of thumb. If the results under certain scenarios would indicate that the funding is too generous (above the range) or too punitive (below the range), the goals or weightings could be adjusted accordingly.

It is important to note that not all goal categories, or goals themselves, lend to execution- and results-based goals. Some goals may only be structured as execution-based goals, and others may only be meaningful when they are results-based.

Conclusion

Aligning pay and performance is central to most compensation philosophies and of upmost importance to investors. Goal selection is critical to building a foundation for this alignment. Compensation committees should strive to avoid paying high or relatively high bonuses based on the scorecard at a time where the stock price falls due to investor views on corporate performance. Results-based goals can build this downside protection into plans providing balance to a set of execution-based goals.