Client Alert | Sep 2020

SEC Mandates Human Capital Disclosure: Nebulous Guidance Provided

New amendments are intended to take into account changes in the regulatory, business, and technological environment since the adoption of Regulation S-K.

As part of an ongoing initiative, the SEC has finalized a new rule that marks an important step to modernize and, in some cases, streamline its disclosure requirements on companies’ business descriptions, legal proceedings, and risk factors. Among the significant changes is a new disclosure rule on how public companies manage their workforce—known as “human capital management” or “HCM”—a much-discussed topic in today’s social climate by investors and the general public alike. The final regulations are effective for the upcoming proxy season in 2021, making it a high priority for compensation committees to have a carefully planned disclosure strategy.

This Client Alert provides context of the disclosure evolution, details as to the precise (albeit abbreviated) final rule, and suggestions as to types of items that may be disclosed.

Background

It has been more than 30 years since the SEC has significantly revised Items 101, 103, and 105 of Regulation S-K, which include a company’s obligation to describe their business, legal proceedings, and risk factors. The amendments adopted in late August 2020 are part of the ongoing Disclosure Effectiveness Initiative led by the SEC to review and improve the effectiveness of its disclosure requirements for the benefit of investors and companies. The amendments are intended to take into account changes in the regulatory, business and technological environment since the adoption of Regulation S-K and put increased pressure on the SEC to require human capital management disclosure.

The rules were finalized after a one-year review of public comment letters following the release of proposed amendments as well as a review of disclosures companies made in response to the COVID-19 pandemic. The final rules were adopted substantially as proposed by the SEC and will be effective 30 days after publication in the Federal Register. As such, some of the amended rules may be relevant for calendar-year companies in preparing their Forms 10‑Q for the quarterly period ending September 30, 2020.

At a high level, major goals of the principles-based amendments include:

- Increased flexibility for companies to tailor the description of their business to their particular circumstances;

- Limited immateriality which eliminates or reduces required disclosure about matters that are not material to an understanding of a company’s business or legal proceedings;

- Streamlined risk disclosure to encourage information that is focused, well-organized, and limited to material risks; and

- Enhanced HCM information that provides material information (in addition to the number of employees, which was already required under the old rule) about a company’s human capital resources.

Out of these four goals, guidance is the scarcest on how to implement the HCM objective. This was criticized by two of the commissioners who dissented to adoption of the principle-based final rules. In explaining her dissent, Commissioner Lee focused on this lack of guidance, pointing out that the SEC received thousands of comments seeking disclosure on workforce development and diversity, which called for both principles-based and prescriptive requirements. She stated that it had never been clearer that investors need information regarding how companies treat and value their employees and how they prioritize diversity in the face of profound racial injustice.

She emphasized that 2020 has highlighted that environmental, social, and governance (ESG) risks, like those associated with diversity, are important predictors for organizational resilience and maximizing risk-adjusted returns on investments. She concluded that she would have supported the final rule if it had “included even minimal expansion on the topic of human capital to include simple, commonly kept metrics such as part-time versus full-time workers, workforce expenses, turnover, and diversity.”

In contrast, SEC Chairman Jay Clayton defended the new rule by taking the position that explicit and inflexible metrics wouldn’t effectively capture differences among companies, which have a wide variety of human capital considerations. Instead, he felt strongly that companies should use their discretion to determine HCM practices that may have a material impact on company performance and on which a reasonable investor may rely in making investment decisions.

Analysis of the New HCM Rule

Previously, the only human capital requirement under Item 101(c) included disclosure on one number: the total number persons employed by the company.

Now, the new rules also require “any human capital measures or objectives that the company focuses on in managing the business.” The rule gives a non-exclusive list of possible items to be considered, but not required for disclosure, including “—depending on the nature of the company’s business and workforce— measures or objectives that address the development, attraction, and retention of personnel.” As is with the case with most SEC disclosures, only material factors need be disclosed.

Notably, “human capital” is not defined because according to the SEC release, the term “may evolve over time and may be defined by different companies in ways that are industry specific.” The release also states that it declined to prescribe human capital metrics which would conflict with SEC efforts to make certain Regulation S-K disclosures more principles-based. Many companies have expressed similar concerns when the rules were proposed in 2019. In letters to the agency last year, many claimed that prescriptive disclosures would be redundant and difficult to make, without a corresponding benefit to investors. These firms also noted that companies already make human capital disclosures in voluntary reports on their websites or in SEC filings when the information is considered material.

While the new rule offers little more than undefined terms and open-ended interpretations, there are some takeaways we can infer from the scant guidance provided.

Materiality: Do not provide human capital disclosure that has immaterial impact on the business or that would not provide information that could be used by a reasonable investor to make investment decisions. For example, if your company has hundreds of thousands of employees and only a handful of part-time or seasonal workers, it may not be relevant to provide the break-out of these types of workers in the larger demographic scheme.

Consider the nature of the company’s business and workforce: Some human capital measures are more important in certain industries than others. Is there something specific about human capital practices that is especially important to your industry or strategy? For example, disclosure about turnover may be less relevant to a large retail company with a large seasonal workforce as compared to a smaller tech company with specialized and critical talent at every level. We expect disclosures will coalesce by industry. As another example, retailers may find the mix between full-time and part-time a material disclosure while traditionally male-dominated industries, such as mining and heavy manufacturing, may focus on gender diversity.

Policies focused on development, attraction, and retention: While this is a non-exclusive list of areas companies may focus on, it is strikingly similar to language often found in the Compensation Discussion and Analysis (CDA) for Named Executive Officers, which frames much of its discussion around compensation. It is possible that Item 101 could turn into a mini-CDA that addresses broad-based compensation strategy and development.

Qualitative and quantitative data will be required: While the rules literally require nothing quantitative other than total number of employees, the SEC Chairman made it clear that they expect companies to provide statistical data to help their shareholders understand their business, and that he expects to see meaningful qualitative and quantitative disclosure.

However and whatever a company decides to disclose, the new HCM transparency (or lack thereof) will be an area of significant voyeurism. It will also be of great interest to activists and other social justice pundits. How selected HCM matters are communicated through disclosure will be critical to framing these issues for employees, competitors, investors and critics.

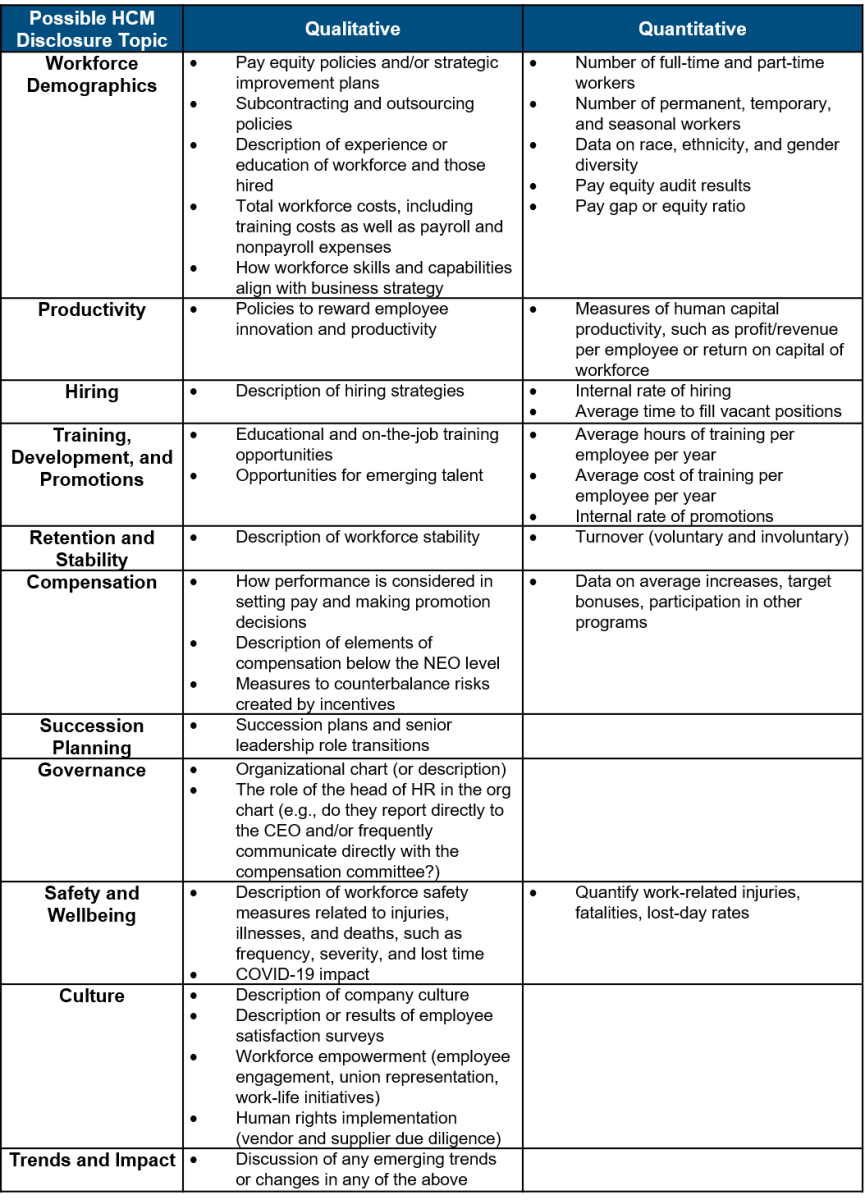

What Could the New HCM Disclosure Look Like?

Beyond the takeaways provided in the literal interpretation of the rules, where should a company begin to determine what will be relevant human capital disclosure for its particular situation?

Below we provide a list of possible areas to explore for materiality. Consider elements that may assist in telling your company’s human capital story and how they may materially impact your business. Only time will tell what categories become overall “best practice” and/or which may be industry specific; however, without any precedent available, the time to start pondering these questions is now.