Article | Jun 2026

Beyond the Debate: The “Last-Minute” Excise Tax Gross-Up

Looking back on a decade of transaction disclosures, the frequency, cost, and voting implications of “last-minute” excise tax gross-ups reveal a practice that remains uncommon but consequential.

Since the late 1990s, shareholders and their advisors have been pressuring companies to eliminate excise tax gross-up provisions from legacy change-in-control (CIC) and severance agreements. Many companies removing gross-ups pledge not to include them in any new agreements going forward.

But despite these commitments, some companies still choose to adopt these agreements ahead of a CIC or other strategic transaction. Recent media attention surrounding a high-profile transaction with newly added excise tax gross-up provisions highlights the continuing relevance of the issue. This is always a sensitive decision for boards, given the vehicle’s poor reputation with shareholders.

In the context of a merger or acquisition, compensation committee members often need answers to the following questions:

- How common is it for companies to agree to new excise tax gross-up protections in the deal context and how costly they are, typically?

- What is the rationale for companies choosing to adopt these?

- Has implementing new excise tax gross-ups impacted corresponding “say-on-golden-parachute” (SOGP) advisory vote results?

To help address these questions, Pearl Meyer analyzed approximately 1,400 SOGP disclosures in transaction filings from January 2016 through December 2025. The results reveal limited activity on “last-minute” excise tax gross-ups, carrying potential implications for boards, executives, and shareholders.

86 Examples of “Last-Minute” Excise Tax Gross-Ups

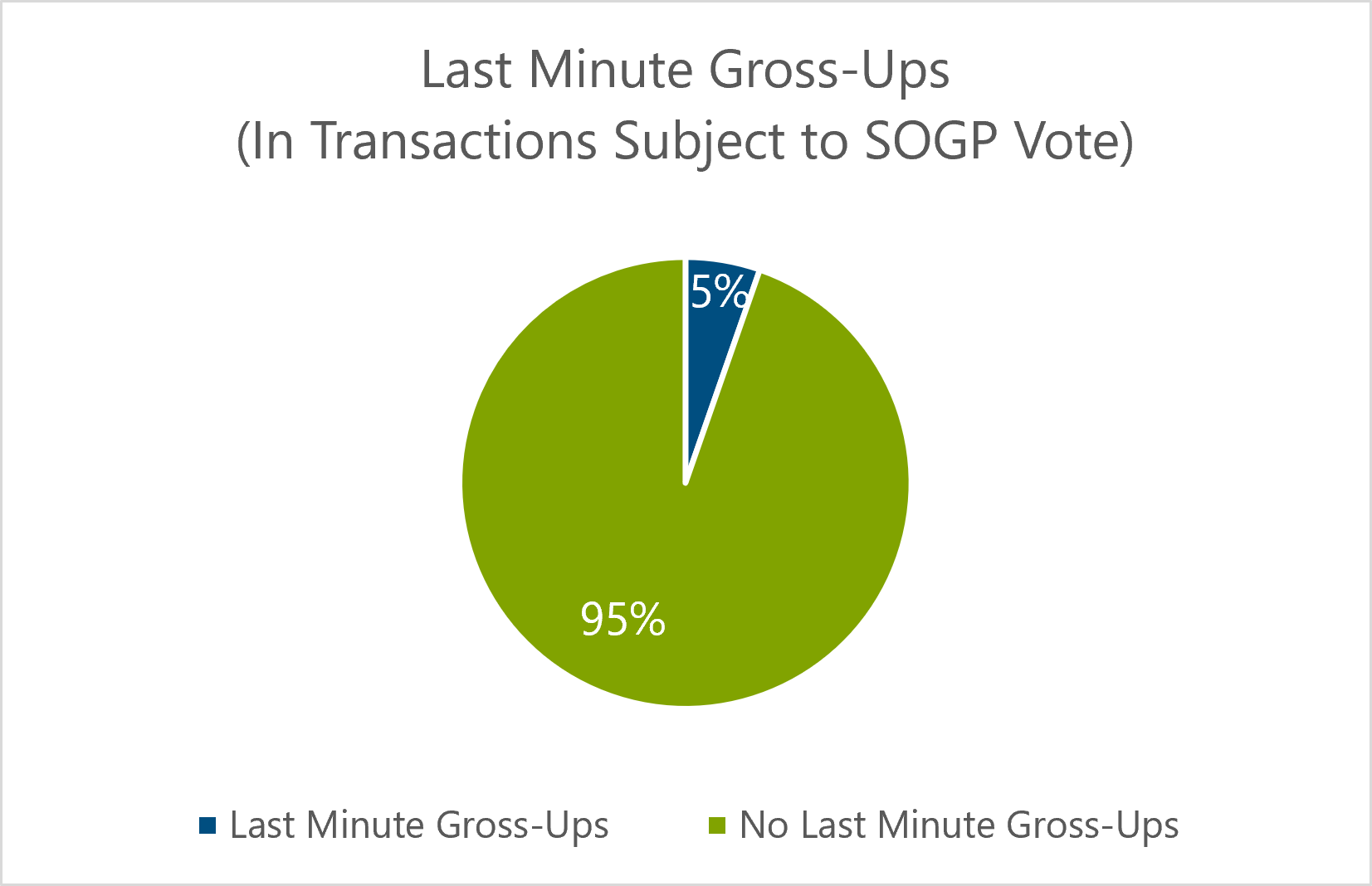

Although providing last-minute gross-ups has grabbed attention, it appears to be a minority practice. Only 6% of the entire study group (5% when considering just the companies subject to a SOGP vote) implemented these at the time of the transaction filing.

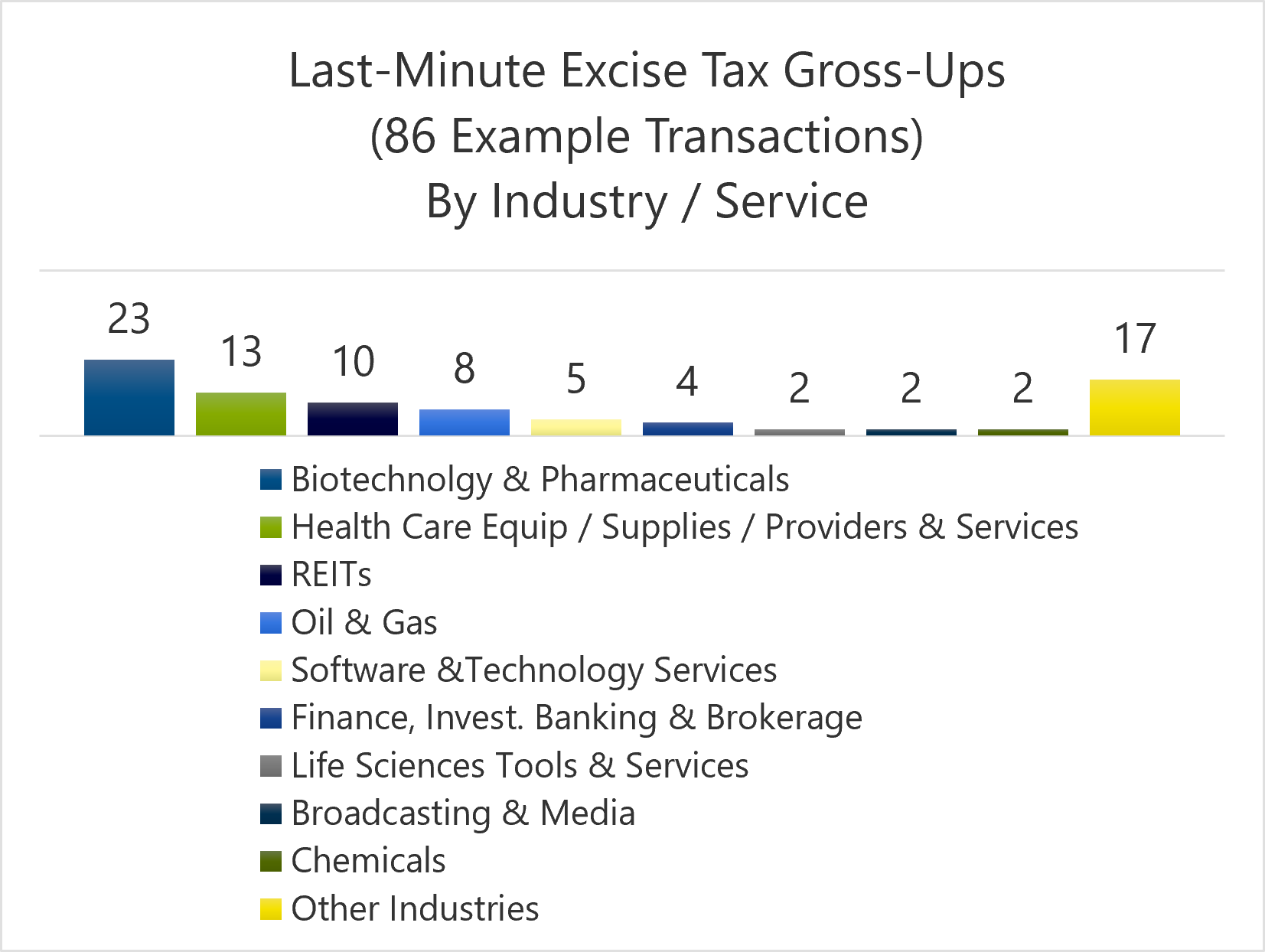

Our study of these transaction disclosures revealed 86 examples of companies (without excise tax gross-up provisions before a CIC) adding one or more of these entitlements shortly before the closing of a transaction—including companies that disclosed the right to provide excise tax gross-ups (to one or more executives) as well as those that actually implemented the entitlements.

Of the 86 companies/transactions, 76 underwent and reported a SOGP advisory vote, while 10 companies were not subject to the vote.

The companies approving last-minute gross-ups spanned various industries and services. Biotechnology/pharmaceutical companies and healthcare equipment and/or service providers had the most instances of implementing them (23 companies and 13 companies, respectively). Of the 10 transactions that were not required to have an SOGP vote, nine were biotechnology companies.1

Deal size doesn’t appear to affect company decisions about providing last-minute gross-ups. Transaction sizes for the 86 companies ranged from $37 million to $73.1 billion; the median and 75th percentile transactions were $4.1 billion and $11.3 billion, respectively.

"Last-Minute” Excise Tax Gross-Ups Transaction Sizes ($mm)2 | ||||

86 Example Transactions: | ||||

Min | 25th Percentile | Median | 75th Percentile | Max |

37 | 1,476 | 4,136 | 11,344 | 73,077 |

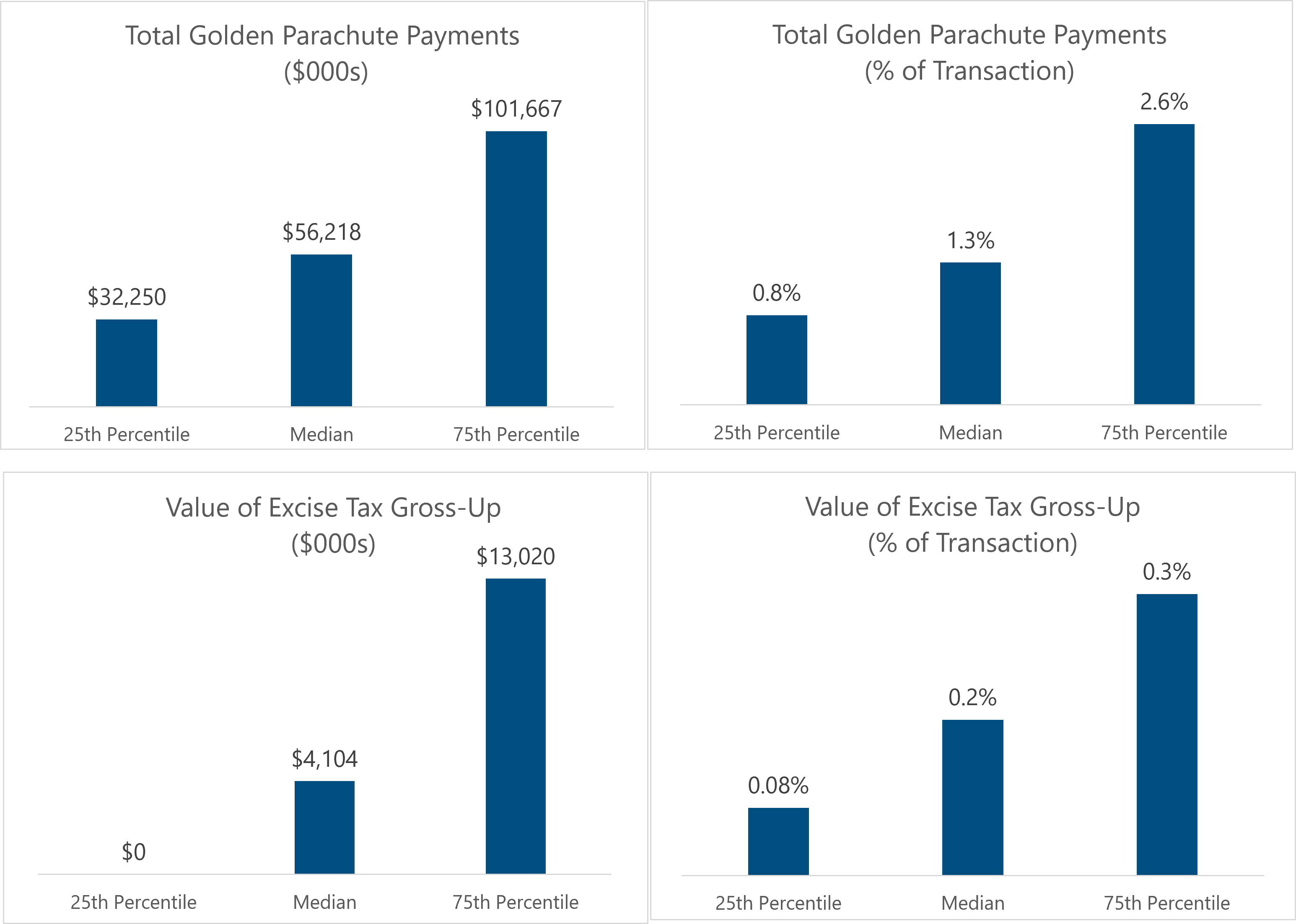

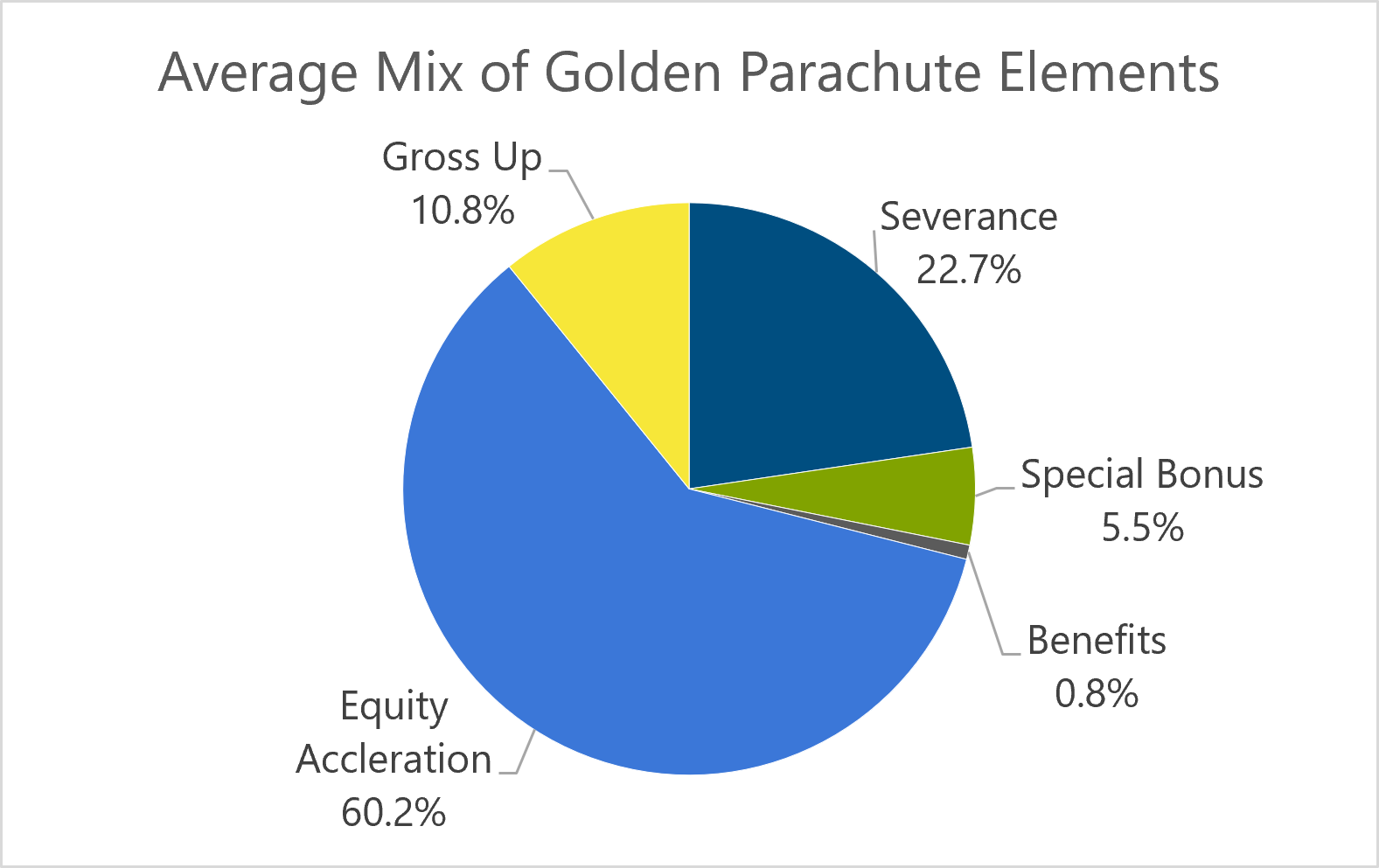

Totals and Types of Golden Parachute Payments

Across the 86 examples, the total amount of golden parachute payments (including excise tax gross-ups) payable to executive officers varied significantly in dollar values relative to a percentage of the transaction value. The value of the excise tax gross-ups provided in these cases also varied substantially.

While the costs of the excise tax gross-ups were significant, they were not nearly as significant as the value of accelerated equity, which represented the largest component of the total golden parachute packages.

Excise Tax Caps

In a likely effort to reduce and fix costs, a little over 50% (44 of the 86 companies) put limits on the total gross-ups they would pay to all executives. These caps ranged from $1 million to $85 million.

Rationale for Implementation

Most companies making last-minute excise tax gross-ups (73%) did not provide reasons for implementing them, perhaps hoping to avoid excessive attention.

Among the minority of companies that offered their insight, we found three common justifications:

- Consideration for Restrictive Covenants: The excise tax gross-up was provided in consideration for entering into a restrictive covenant agreement where executives would be subject to non-competition and non-solicitation provisions for a period of time after the transaction and their terminations.

- Alignment with Shareholders: The value of equity acceleration, driven by the deal price negotiated by executives, represented the majority of the golden parachute payments. Securing the best price was in the best interests of shareholders, and the 280G excise tax imposed on executives was punitive compared to the ultimate value delivered to shareholders.

- Retention: Special arrangements were needed to retain key executives during the transition period following the CIC.

Impact of Last-Minute Gross-ups on SOGP Vote Results

As mentioned, in 10 of the companies that had implemented 280G gross-ups, no advisory SOGP vote was required in the transaction process.

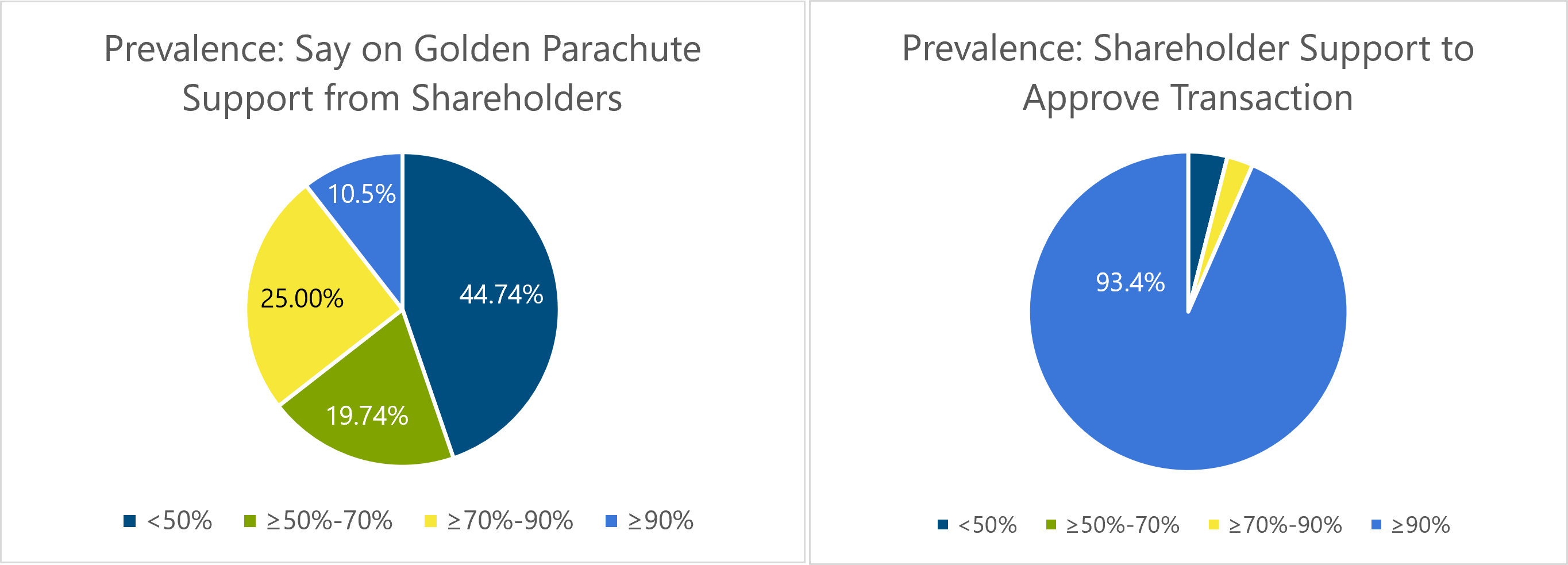

However, in the remaining 76, the transaction required a shareholder vote. In these transactions, shareholders were much less supportive of the golden parachute payments than they were for the transactions themselves: just under 90% of the companies received less than 90% support in the SOGP vote—in fact, just under half (44%) of the companies failed to receive 50% support. Conversely, shareholders provided overwhelming support for the overall transactions. The average vote to approve a transaction in this group was 98%.

Given these results, boards approving new excise tax gross-ups should be well aware that the SOGP advisory vote may ultimately fail.

Conclusions

Only 5% of companies in the transaction study group subject to SOGP votes implemented excise tax gross-up provisions in connection with impending transactions, with biotechnology/pharmaceutical companies and healthcare equipment and/or service providers having the most instances of implementation. However, most of the companies in the study group (95%) did not provide any new gross-up protection.

When approved, excise tax gross-up costs (as a dollar value and as a percentage of the transaction value) were significant. As a means of limiting and fixing the associated liabilities, many companies have disclosed dollar limits on the protections provided. Notably, however, excise tax gross-ups were generally not the largest component of executive transaction payouts. In most cases, accelerated equity awards accounted for the majority of total golden parachute value.

Just under half of the example companies that implemented last-minute gross-ups failed the SOGP advisory vote. Despite the negative repercussions, SOGP disclosures provide a glimpse into the reasoning for the minority of companies that approved them. In the transaction setting, excise tax gross-ups have served as consideration for non-compete restrictions, retention vehicles, and a means to align management with shareholder outcomes.

An additional explanation for the varying practices may relate to an organization’s history. Mature, stable organizations are better able to thoughtfully plan for CIC contingencies; their executives are also more likely to have received the benefit of short- and long-term incentive payouts, thus improving their 280G results. High-growth companies, by contrast, may have limited historical compensation, increasing the likelihood that executives will owe 280G excise taxes. For boards of these companies, inaction might be viewed as punitive to the executives who have created significant shareholder value.

The decision on whether to provide an excise tax gross-up is sensitive, and companies implementing them should expect heightened shareholder scrutiny and lower SOGP support levels. In addition, legal advisors may express concerns that implementing these types of provisions may further encourage shareholder lawsuits that so often accompany transactions. Boards must weigh whether the benefits to shareholders will ultimately outweigh the costs as part of their fiduciary oversight.

1One pharmaceutical company was also not subject to the SOGP vote.

2Transaction equity values as reported by Capital IQ.