Article | Jun 2026

For Tech Companies That Have Gone Vertical, Boards Should Be Discussing Four Key Talent and Pay Issues with Management

The AI boom has created enormous shareholder and employee wealth, but boards now face a new set of questions about pay calibration, retention, goal setting, and succession planning as growth inevitably normalizes.

Over the last 36 months, we have seen the AI build-out gather momentum, starting with OpenAI and its development and deployment of ChatGPT, Nvidia supplying GPUs, and other household names adopting the technology in various ways across different businesses. However, today the broader AI build-out has affected a significant portion of the technology industry and global economy.

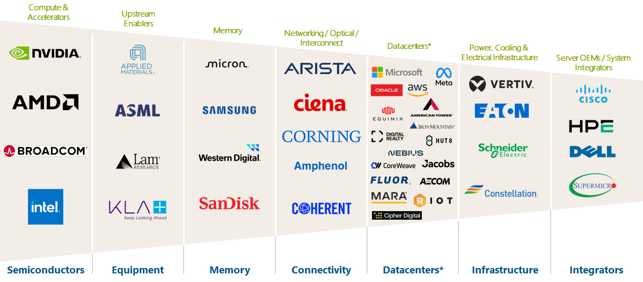

To better understand the talent and compensation implications of the AI build-out, we analyzed 43 companies across the AI value chain, including semiconductor manufacturers, equipment providers, memory companies, networking and connectivity providers, data center operators, infrastructure companies, and systems integrators. Our review focused on shareholder returns, valuation multiples, executive compensation outcomes, and leadership demographics over the past five years.

Significant Value Creation Across the AI Value Chain

As shown below, the AI value chain extends beyond household names to include critical infrastructure and energy companies, which are being swept in at the tail end of the build-out.

Note: *The data center sample includes companies that operate in the following subcategories: colocation/data center REIT space, hyperscaler-owned data center operators, neoclouds, GPU-as-a-Service, and bitcoin miners pivoting to data center builds.

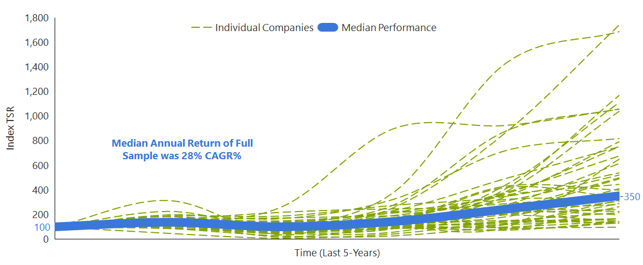

The AI build-out has led to a number of these companies’ total shareholder return (TSR) going vertical in the last 24–36 months, resulting in significant wealth creation for executive teams and talent who joined before the market momentum started.

AI Value Chain Sample Indexed TSR (December 2020–May 2026)

Note: Indexed TSR is the cumulative return of each company (change in share price + reinvestment of dividends) from December 2020 through May 2026.

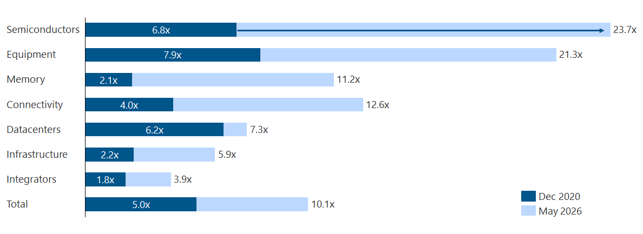

For most, valuation multiples have at least doubled across the AI value chain in the last five years.

Enterprise Value to Revenue Multiple (December 2020–May 2026)

While the magnitude of value creation varies across segments of the AI ecosystem, this analysis revealed several similar talent and pay dynamics that will evolve in the years ahead. We believe the four common topics that boards and compensation committees should be actively discussing include:

- Calibrating pay appropriately after significant wealth creation.

- Managing future employee earnings and retention.

- Setting performance goals in rapidly expanding markets.

- Preparing for potential succession challenges as leaders become retirement-eligible earlier than expected.

1. Calibrating Pay

Compensation committees should be asking:

- How should peer group development evolve as the industry landscape shifts materially?

- Is market capitalization the right size metric to anchor on?

- Are pay levels appropriately calibrated going forward?

- Do we orient pay decisions on ‘target’ pay or ‘realized’ outcomes to ensure alignment with competitive pay levels and performance?

Given the diverse size of these companies, differing pay designs (e.g., multi-year awards vs. annual target pay, founder vs. non-founder status), and where they compete in the value chain, it is often difficult for boards and Committees to calibrate what is appropriate.

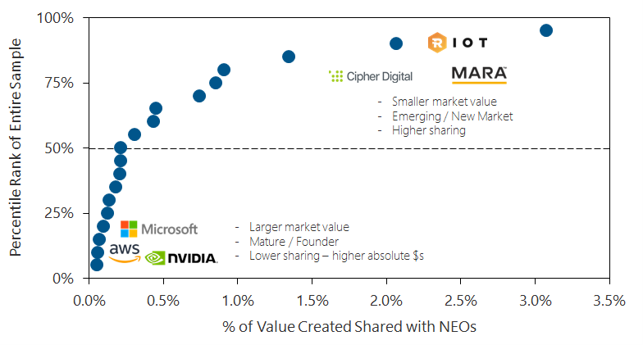

Our work with high-growth organizations suggests that a more appropriate and somewhat “innovative” approach is to consider both target pay opportunities, realized outcomes, and sharing rates (either as a percentage of market value or of market value created over a defined period). Doing so helps provide a secondary lens to double-check the question: Are we paying competitively and appropriately after normalizing for pay program differences?

In reviewing the sample above, our research suggests that the aggregate incremental sharing rate for named executive officers (NEOs) over the last 5 years (actual cash + vested value of RSUs/PSUs and exercised options) has generally been within a quarter point (0.25%) and 1.0% of the incremental value created.

Our analysis shows that sharing rates align with historical norms. However, still-emerging segments of the value chain are receiving a premium. For purposes of this analysis, the sharing rate is defined as realized NEO compensation (cash compensation, vested equity value, and option exercises) divided by incremental shareholder value created from December 2020 to May 2026.

Sharing Rates Across the AI Value Chain in $Billions (December 2020–May 2026)

Segment | Aggregate Incremental Value Created | Aggregate NEO Value Realized | % Sharing |

Semiconductors | $7,864.8 | $5.6 | 0.07% |

Equipment | $784.7 | $1.3 | 0.16% |

Memory | $913.0 | $0.9 | 0.09% |

Connectivity | $575.1 | $2.1 | 0.36% |

Datacenters | $7,352.4 | $9.7 | 0.13% |

Infrastructure | $223.5 | $0.4 | 0.20% |

Integrators | $476.6 | $1.5 | 0.31% |

Total | $18,190.2 | $21.4 | 0.12% |

Median | $139.8 | $0.3 | 0.25% |

Top-Quartile Sharing Rates Are Substantially Higher (December 2020–May 2026)

2. Managing Future Employee Earnings/ Expectations

Compensation committees should be asking some challenging questions:

- How are we going to ensure appropriate holding power is in place, while also managing a drop in employee earnings as performance normalizes in future years?

- Philosophically, are we prepared to act as a board and management team proactively to address any potential retention concerns?

- Will we apply the same approach to all affected or be willing to segment our population to address more acute issues (e.g., longer-tenured employees vs. new hires)?

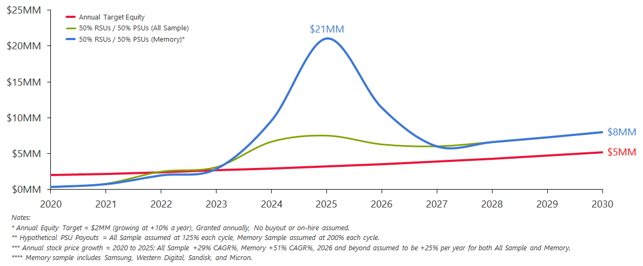

Regardless of whether future performance remains strong, with stock prices up 5x, 10x, or 15x in the last 36 months, there will be a significant wealth-creation event followed by a dramatic drop in employee earnings. We believe proactively planning today for these looming events is an important task for many of these Committees over the next 1–3 years. They will need to be willing to develop bespoke pay programs tailored to specific talent cohorts, or even down to the individual level, for people who can execute.

For example, the use of long-tailed RSUs (i.e., a 0%, 0%, 20%, 40%, 40% vesting schedule), or boxcar grants that vest 100% in years 4 or 5. Bespoke performance grants tied to specific AI milestones, etc. Boards will need to become comfortable stepping outside the norm to address their company-specific context.

This is illustrated in the graphic below, showing the hypothetical payout of equity values through 2030. Even with strong performance, managing the looming cliff at some of these organizations will require careful consideration, planning, and creative thinking.

Hypothetical Payout of Equity Values in $Millions

3. Goal Setting

Rapid industry expansion also creates another challenge: Establishing performance goals that remain rigorous while accounting for a dramatically changing market opportunity. Some of the key questions are:

- How do we set appropriate performance goals for either our annual plan or PSUs when the industry TAM is shifting materially?

- Are certain performance metrics or performance periods better to use in periods of rapid growth over others?

- Are relative metrics more appropriate to use when entire markets/ industries are rising?

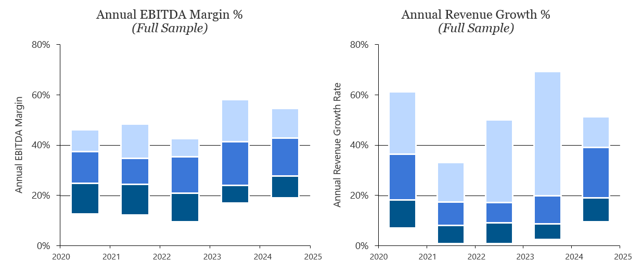

We looked at various performance metrics (growth, return, and margin) across the sample companies. Consistent with our work with high-growth industries and companies, certain performance metrics will behave differently. When working with these high-growth companies (i.e., those creating new categories or new markets), there are four important principles to follow:

- Agree on a general framework for how often payouts should be at threshold, target, and maximum. Ensure this aligns with the stated pay philosophy. Under normal circumstances, the target should be achieved 50–60% of the time, while the maximum is expected 10–20% of the time. Organizations in the AI ecosystem should consider whether the outcomes should follow historical norms or be adjusted. The answer to this question will depend on each company’s perspective/ philosophy and will impact the goal-setting discussion.

- Start by ensuring the target is aligned with the board-approved budget. However, allow some flexibility in the decision-making system to account for the fact that forecasting in this environment can be challenging.

- Create performance ranges (threshold to maximum) that are grounded in the current market context but provide the necessary stretch that aligns with shareholder performance expectations and the probability of potential business outcomes discussed in point #1 above.

- Clearly define an adjustment framework upfront to provide the Committee with ample latitude at the end of the year.

Different Performance Metrics Will Behave Differently

Margins tend to be less volatile and remain within a range than top-line or bottom-line growth metrics.

4. Succession Planning

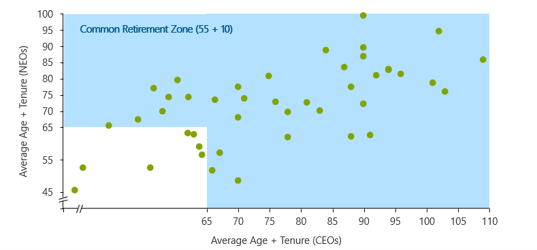

Since most CEOs and NEOs are in the retirement zone, boards should anticipate potential succession risks in the near- to medium-term. They should be asking:

- Do we have succession plans in place at the executive level and two levels below, including those critical to winning in the new AI era?

- If not, what are we as a board actively doing to accelerate those plans, knowing that critical retirements will hit the industry over the next 5 years (executives will age out or retire due to significant wealth creation)?

Our research examined NEOs at the 43 companies in our sample and found that a significant portion of those in leadership positions today would likely already meet a common definition of retirement (i.e., 55 years old and 10 years of service).

Boards and Committees across these companies should be actively considering how to create programs to help retain critical talent (executives and those needed to win once the build-out is complete) through the retirement eligibility period (either 55+10 or 60+5). Special equity programs that are excluded from standard retirement treatment and cliff vesting in the outer years can be an effective way to ensure the right bench strength stays in place.

Age & Tenure Among CEOs and NEOs

Looking Ahead

The AI build-out has created extraordinary shareholder returns, significant employee wealth, and new competitive pressures across the technology ecosystem, but this isn’t the first time we have seen this type of meteoric growth. The dot.com era and the COVID surge were both characterized by similar dramatic rises in company valuations followed by a period of normalization. While it remains to be seen how the AI build-out will play out in the tech sector and broader economy, boards and compensation committees can actively plan now for future changes to pay calibration, retention, goal setting, and succession planning.

There is no one-size approach to pay and talent going forward. The challenge for most boards and compensation committees goes beyond pay-for-performance to maintaining motivation, retention, and alignment after significant wealth has already been created. Committees should be willing to step outside market norms, customize, and plan—so that when needed, the chosen strategy has been appropriately stress-tested and will be durable through the next phase of the AI buildout.