Article | Apr 2026

Oilfield Services 2026 Proxy Season: Early Return Compensation Insights

Early 2026 proxy disclosures show oilfield services companies balancing stronger incentive outcomes with continued restraint on fixed pay amid ongoing market uncertainty.

Early proxy disclosures from oilfield services (OFS) companies suggest that 2025 results led to moderate improvements in incentive outcomes. While annual and long-term incentive (LTI) payouts generally rebounded, companies remained measured in adjusting fixed compensation, reflecting persistent macroeconomic uncertainty and volatility across the sector.

This analysis reviews CEO compensation trends across 15 OFS companies, with revenues ranging from approximately $600 million to $36 billion. We focus on three areas: base salary adjustments, annual and LTI outcomes, and the implications for compensation design heading into 2026.

Base Salaries Remain Restrained, Reflecting Focus on Performance

CEO base salary adjustments remained conservative in 2025, with a median increase of 3% and 40% of companies reporting no change. While higher than the modest 2024 increase (0.6%), salary movement continues to lag historical norms, reinforcing the sector’s cautious approach to fixed compensation.

Notably, base salary changes showed limited differentiation across companies, with no clear pattern based on size, performance, or business mix. Even among companies delivering above-target incentive outcomes, base salary increases were generally restrained.

This reinforces a broader trend: companies are prioritizing variable, performance-based compensation over fixed cost increases to preserve flexibility amid limited visibility.

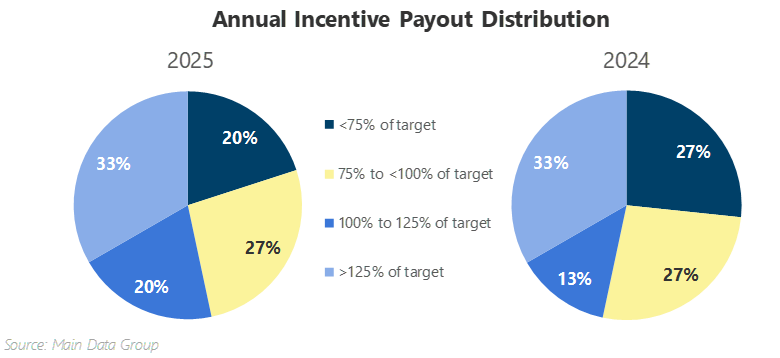

Annual Incentives Outcomes Improve, but Vary by Revenue Source

Annual incentive outcomes rebounded in 2025, with median payouts rising to 115% of target (from 95% in 2024). However, results varied across the sector, driven largely by differences in business mix and exposure to key end markets. Companies with greater exposure to offshore and longer-cycle project activity generally delivered stronger results. Companies tied to power, infrastructure, and gas-related services also reported above-target payouts, supported by strong demand for energy infrastructure and operational reliability.

In contrast, companies more heavily exposed to North American short-cycle activity—particularly those tied to drilling, completions, and pressure pumping—experienced more mixed or below-target outcomes.

It is important to note that payout dispersion remained within each of these two groups, as company-specific execution, cost management, and goal calibration also played a significant role in determining outcomes.

| Above-target payouts were generally concentrated among companies exposed to offshore and power/infrastructure markets (average ~149% of target), while North American short-cycle–oriented businesses saw more muted outcomes (average ~88% of target). |

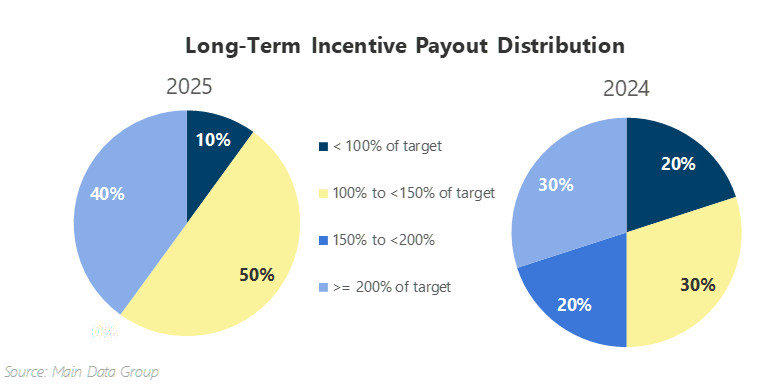

LTI Awards Increase Modestly as Payouts Normalize from 2024 Highs

LTI awards increased modestly in 2025, with 53% of companies reporting higher target grant values with a median increase of 5%. Payout outcomes tell a more nuanced story.

Among companies reporting payouts for performance-based LTI cycles ending in 2025, 90% delivered above-target payouts, with a median payout of 133%. While still elevated, this represents a decline from the 2024 median of 152%, indicating early signs of normalization following exceptionally strong prior-cycle performance. These outcomes reflect the lagged nature of LTI programs, with payouts still benefiting from stronger prior-cycle performance.

| Larger companies ($2.5B in revenues or more) outpaced the broader group in LTI payouts, with higher grant increases (median +7%) and stronger payout levels (144% of target), reinforcing a continued scale advantage in both performance and pay positioning. |

2026 Outlook: Flexibility and Operational Metrics Take Priority

The 2026 proxy season reflects a sector balancing improved performance with ongoing uncertainty. Practices introduced in response to recent volatility, such as wider performance ranges and increased weighting of operational measures, are becoming more embedded in compensation design. In particular, we expect continued emphasis on metrics that management can more directly influence, including cost control, capital efficiency, and operational reliability, as companies navigate reduced visibility into commodity-driven financial outcomes.

In a sector defined by cyclicality and structural change, compensation programs that balance metric expansion with clear pay-for-performance alignment will be best positioned to support talent retention and shareholder expectations.