Article | Jun 2026

How Employers Are Managing Healthcare Costs in 2026: Findings from Pearl Meyer’s Latest Benefits Survey

New research reveals how employers are balancing rising costs, evolving workforce expectations, and competitive talent pressures through changes to their benefits programs.

Rising healthcare costs continue to reshape employer benefits strategies. As organizations balance healthcare affordability with the need to offer competitive benefits programs, many are reevaluating their health plan designs, cost-sharing strategies, and wellness offerings.

Findings from the 2026 Pearl Meyer Benefits and Human Resources Policies Survey reveal that employers are taking a multifaceted approach to managing benefits expenses. Rather than relying on just one solution, organizations are combining plan design changes, high-deductible health care plans (HDHPs), wellness initiatives, and self-insurance to address increasing costs while trying to maintain competitive benefits offerings.

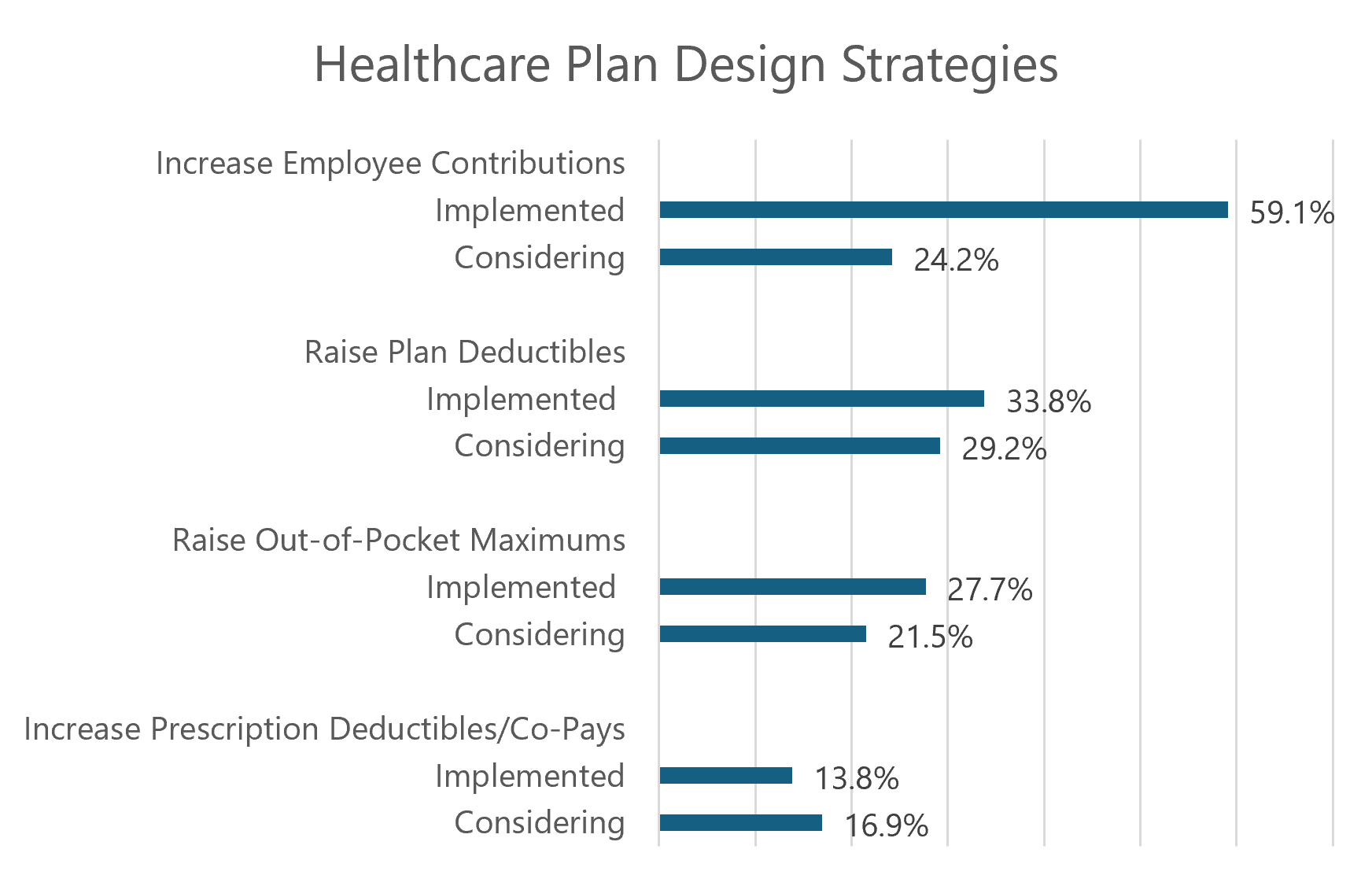

Cost Sharing Remains a Primary Strategy

One of the most common approaches employers have adopted is increasing employee cost-sharing for healthcare coverage. Nearly 60% of organizations in the survey reported that they had increased employee contributions to healthcare premiums in or before 2025. Looking ahead, an additional 24.2% are considering increasing employee contributions during 2026 or 2027.

Employers have also adjusted plan design features to help manage costs. More than one-third of organizations (33.8%) have already raised plan deductibles, while 29.2% are considering doing so in the next two years. Similarly, 27.7% have increased employee out-of-pocket maximums, and 21.5% are considering future increases.

Prescription drug costs are also a focus area. Nearly 14% of organizations have already increased prescription deductibles or co-pays, while another 16.9% are evaluating this option.

These findings highlight the balancing act many employers face as they seek to manage rising healthcare costs through higher employee contributions, increased deductibles, and other plan design changes while maintaining competitive benefits programs.

HDHPs Remain a Common Approach to Healthcare Cost Management

HDHPs remain a common feature of many employer healthcare strategies. Among participating organizations, 73.6% offer a high-deductible PPO plan, making it nearly as prevalent as the traditional PPO plan, which 81.3% offer. In fact, 60.9% of employers reported having already implemented a high-deductible health plan as part of their cost-management strategy.

The financial differences between traditional PPOs and HDHPs highlight the tradeoffs associated with these plan designs. While the average monthly premium is lower for an HDHP, employees typically face higher deductibles. To offset some of these costs, many employers contribute to health savings accounts (HSAs). Nearly half of organizations (46.7%) that offer HDHPs also contribute to employee HSAs. The chart below illustrates how this plays out, using employee + family coverage as an example.

Employee + Family Health Plan Coverage Comparisons (2026) | ||

| HDHP PPO | Traditional PPO | |

| Average monthly premium | $2,220 | $2,564 |

| Average deductible | $5,679 | $2,491 |

| Average employer HSA contributions | $1,486 | n/a |

These findings suggest that many employers continue to view HDHPs as a long-term component of their healthcare strategy, while employer HSA contributions help offset some of the higher potential upfront costs employees face.

Self-Insurance as a Healthcare Cost Management Approach

Self-insurance is another approach organizations use to structure and finance their healthcare programs. More than 75% of participating organizations reported that their primary healthcare plan was self-insured. Under a self-insured arrangement, employers assume direct responsibility for healthcare claims rather than purchasing a fully insured health plan from an insurance carrier.

To manage the financial risks associated with self-funding, most organizations purchase stop-loss protection. Among employers with self-insured plans, 44.1% maintain stop-loss coverage for high individual claims, while an additional 48.5% maintain coverage for both high individual and aggregate claims.

The average stop-loss threshold for individual claims is $336,404, and the average aggregate stop-loss threshold is $696,729. These arrangements help protect organizations from unusually large claims while allowing them to retain many of the advantages associated with self-funded healthcare plans.

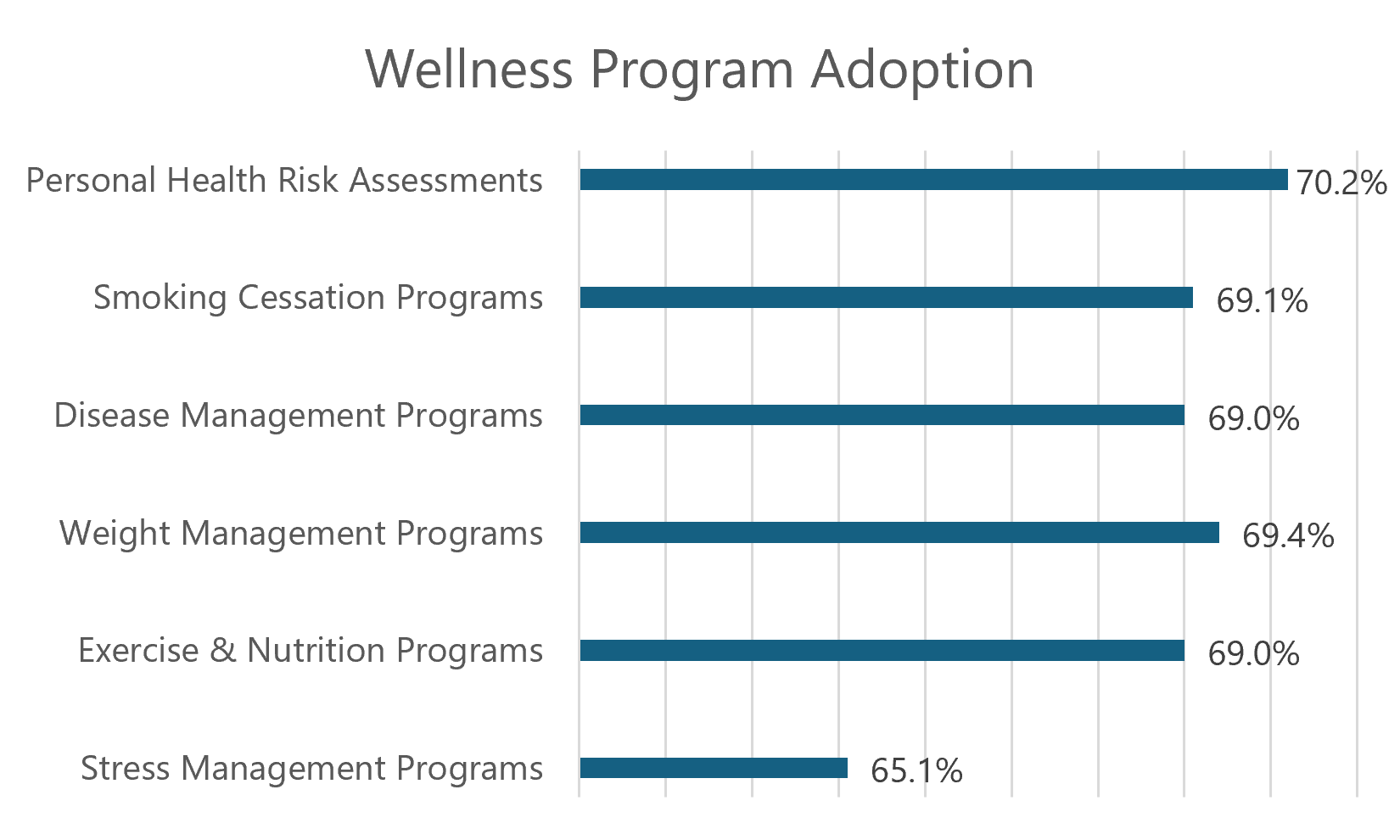

Wellness Programs Are a Key Investment Area

While plan design changes receive significant attention, many employers are also investing in programs designed to improve overall employee health and wellbeing, potentially reducing future healthcare costs.

More than two-thirds of organizations offer the following programs:

In addition, 59.3% provide health fairs or wellness seminars.

Many organizations also encourage participation through incentives. More than half (57.1%) offer rewards for wellness program participation, with the average financial incentive totaling $446.

A meaningful number of organizations also offer lifestyle reimbursement programs. Nearly half of organizations (45.7%) already offer wellness-related reimbursement programs, and another 12.3% are considering implementing them in the future.

These findings suggest that employers view wellness programs as a long-term strategy for improving workforce health and potentially reducing future healthcare expenditures.

Emerging Areas of Coverage Reflect Changing Employee Needs

One notable finding is the coexistence of cost containment and expanded benefits. While many employers continue to increase employee cost sharing, they are also broadening access to services such as virtual primary care, infertility treatment, and obesity management. The data suggest that organizations are making increasingly selective decisions about where to reduce costs and where to expand benefits.

Participating organizations report offering coverage for a broad range of healthcare services beyond traditional medical care, reporting:

- 54.4% cover infertility treatments

- 46.8% cover weight loss or obesity treatments

- 39.2% cover GLP-1 medications

- 36.7% cover gender reassignment services

- 35.4% cover genetic testing

- 86.1% provide virtual primary care services

Coverage decisions for obesity treatments and GLP-1 medications show the difficult tradeoff employers face when considering attractive benefits offerings for their employees. While these treatments may improve employee health outcomes, they can also represent a significant healthcare expense. Organizations must weigh employee demand against cost considerations.

Looking Ahead

While healthcare remains one of the most significant drivers of benefits costs, our survey findings suggest that employers are taking a more strategic and integrated approach to benefits design. Rather than relying on a single cost-management strategy, organizations are combining plan design changes, funding approaches, wellness investments, and evolving coverage offerings to support both financial sustainability and the employee experience.

As workforce expectations continue to evolve and benefits costs remain under pressure, employers will need to regularly assess whether their programs align with organizational priorities, support employee wellbeing, and strengthen their ability to attract and retain talent in a competitive market.

The 2026 Pearl Meyer Benefits and Human Resources Policies Survey provides extensive further benchmarking and insights on healthcare, paid time off, leave policies, health and welfare programs, and other key benefits to help organizations evaluate and refine their total rewards strategies.

Methodology

The survey included over 400 questions on benefits, perquisites, and HR policies, answered by 92 participating companies. All reported data reflect responses from only the firms that offer a particular benefit, perquisite, or program. The full survey report includes answers to questions for which there was sufficient data to report, with a minimum of 3 responses.